Cheap Auto Insurance After a DUI in 2025 (Top 10 Low-Cost Companies)

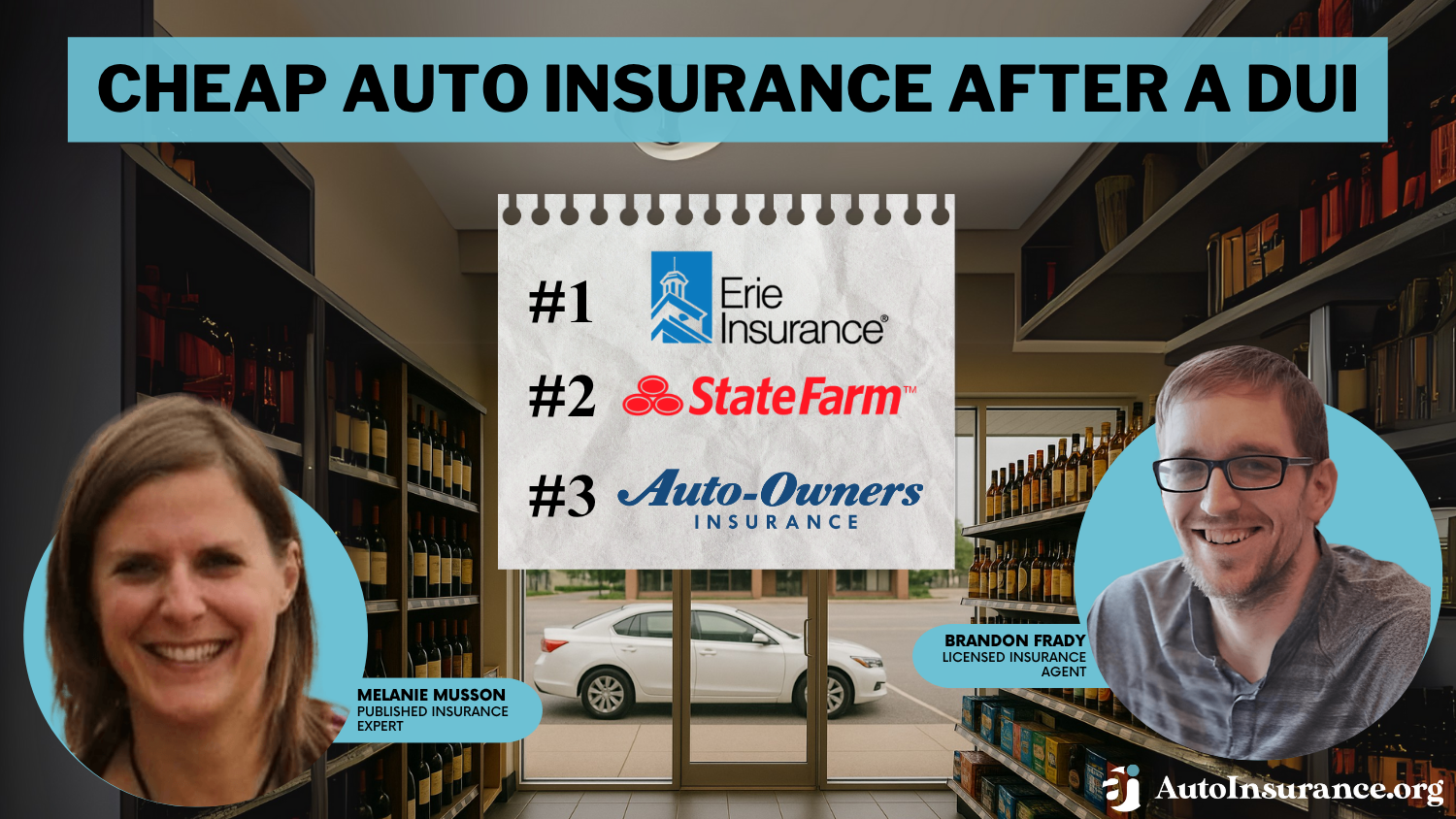

Erie, State Farm, and Auto-Owners sell cheap auto insurance after a DUI. Erie has the best DUI insurance rates at $42/mo but is only available in 12 states. State Farm has the cheapest rates nationally, at $45/mo. Auto insurance rates for drivers with a DUI average 74% higher than drivers with clean records.

Free Car Insurance Comparison

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Brandon Frady

Licensed Insurance Agent

Brandon Frady has been a licensed insurance agent and insurance office manager since 2018. He has experience in ventures from retail to finance, working positions from cashier to management, but it wasn’t until Brandon started working in the insurance industry that he truly felt at home in his career. In his day-to-day interactions, he aims to live out his business philosophy in how he treats hi...

Licensed Insurance Agent

UPDATED: May 27, 2025

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident auto insurance decisions. Comparison shopping should be easy. We are not affiliated with any one auto insurance provider and cannot guarantee quotes from any single provider. Our partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

Editorial Guidelines: We are a free online resource for anyone interested in learning more about auto insurance. Our goal is to be an objective, third-party resource for everything auto insurance related. We update our site regularly, and all content is reviewed by auto insurance experts.

UPDATED: May 27, 2025

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident auto insurance decisions. Comparison shopping should be easy. We are not affiliated with any one auto insurance provider and cannot guarantee quotes from any single provider. Our partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

On This Page

1,883 reviews

1,883 reviewsCompany Facts

Monthly Rate for DUI

A.M. Best

Complaint Level

Pros & Cons

1,883 reviews 18,155 reviews

18,155 reviewsCompany Facts

Monthly Rate for DUI

A.M. Best

Complaint Level

Pros & Cons

18,155 reviews 563 reviews

563 reviewsCompany Facts

Monthly Rate for DUI

A.M. Best

Complaint Level

Pros & Cons

563 reviewsErie is the cheapest auto insurance company after a DUI with monthly minimum rates as low as $60.

Finding auto insurance for drivers with a DUI can be difficult, though many high-risk auto insurance companies offer affordable coverage. State Farm has the cheapest rates in more states than Erie, starting at $60/mo. Auto-Owners offers big bundling discounts to homeowners on top of cheap rates after a DUI.

Top 10 Company Picks: Cheap Auto Insurance After a DUI

| Company | Rank | DUI Rates | Low-Mileage Discount | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | $60 | 30% | Customer Service | Erie | |

| #2 | $65 | 30% | Many Discounts | State Farm | |

| #3 | $72 | 30% | Coverage Flexibility | Auto-Owners | |

| #4 | $75 | 30% | Budgeting Tools | Progressive | |

| #5 | $93 | 10% | Exclusive Benefits | The Hartford | |

| #6 | $104 | 20% | Costco Members | American Family | |

| #7 | $112 | 20% | Discount Options | Travelers | |

| #8 | $129 | 20% | Deductible Options | Nationwide | |

| #9 | $152 | 30% | UBI Savings | Allstate | |

| #10 | $178 | 30% | Safe-Driving Discounts | Liberty Mutual |

A DUI significantly impacts auto insurance quotes, causing an average increase of 74%. Still, some companies offer cheap DUI insurance to drivers looking for affordable rates. Compare quotes online to find the best cheap auto insurance after a DUI.

- Erie, State Farm, and Auto-Owners have cheap auto insurance after a DUI

- Auto insurance for drivers with a DUI costs 74% more on average

- Get cheap DUI auto insurance by comparing quotes from various companies

#1 – Erie: Cheapest Overall

Pros

- Erie Rate Lock: Rates won’t change after a claim or policy changes

- SR-22 insurance: Erie files SR-22 after a DUI, including non-owner SR-22

- Diminishing deductibles: Erie reduces deductibles by $100 every year you don’t file a claim

- Great customer service reviews: Get full rankings in our Erie auto insurance review

Cons

- Limited availability: Only in 12 states

- Fewer discounts: Erie doesn’t offer common discounts you’ll get at other companies, like low-mileage

Free Auto Insurance Comparison

Enter your ZIP code below to view companies that have cheap auto insurance rates.

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

#2 – State Farm: Cheapest for SR-22 Coverage

Pros

- SR-22 insurance: State Farm files SR-22 after a DUI, including non-owner SR-22

- Cheapest rates in more states: Affordable State Farm auto insurance in 48 states. Find cheap coverage near you in our State Farm review.

- Big low-mileage discounts: Save up to 30% when you drive less than 10,000 miles per year.

- Great claims satisfaction: Top five company in annual J.D. Power survey.

Cons

- No gap insurance: Only provides Payoff Protector on auto loans originated from State Farm Bank

- Model restrictions: State Farm is no longer insuring certain Kia and Hyundai models.

#3 – Auto-Owners: Cheapest for Homeowners

Pros

- Multi-policy discounts: Drivers who have home or life insurance policies with Auto-Owners qualify for a discount. Discover more discounts in our Auto-Owners insurance review.

- Common loss deductible: Homeowners get reduced or waived auto insurance deductibles if both their home and car are damaged in a covered event.

- Great claims satisfaction: Top ten company in annual J.D. Power survey

Cons

- No SR-22 filings: Doesn’t file SR-22 insurance after a DUI

- Limited availability: Only in 26 states

#4 – Progressive: Cheapest for Accident-Free Drivers

![]()

Pros

- SR-22 insurance: Progressive files SR-22 after a DUI, including non-owner SR-22

- Deductible Savings Bank: Reduces auto deductibles by $100 every year you remain claim-free

- Forgiveness for small accidents: Progressive never raises rates after a first claim as long as it’s under $500. Learn more in our Progressive insurance review.

Cons

- Poor customer service: Below-average for claims and customer service in multiple regions

- High rates for young drivers: Drivers under 25 pay more after a DUI than with other companies

Free Auto Insurance Comparison

Enter your ZIP code below to view companies that have cheap auto insurance rates.

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

#5 – The Hartford: Cheapest for Seniors

Pros

- Senior driver discounts: AARP members get exclusive savings offers and discounts. Compare rates and discounts in The Hartford auto insurance review.

- Legal assistance included: Auto policies cover a lawyer if you need one after an accident

- Recover Care coverage: Covers home care costs, like cleaning services, while you recover from an accident

Cons

- High rates for young drivers: Drivers under 25 pay more after a DUI than with other companies

- Below average customer service: Other national insurers have higher customer and claims satisfaction

#6 – American Family: Cheapest in the Central Midwest

Pros

- Big discounts for homeowners: Save 25% with a multi-policy discount

- SR-22 insurance: Files SR-22 after a DUI, including non-owner SR-22

- Great claims satisfaction: Top ten company in annual J.D. Power survey

- Above-average customer satisfaction: Ranks among the top companies in its region for customer service

Cons

- Limited availability: Only in 19 states. Use our American Family review to find coverage near you.

- Expensive with bad credit: Drivers with bad credit can find cheaper rates with other companies

#7 – Travelers: Cheapest With a New Car

Pros

- New car discounts: Earn a discount for insuring vehicles less than three years old

- New car replacement: Policy add-on to replace totaled vehicles less than five years old and cover gap insurance payments

- SR-22 insurance: Files SR-22 after a DUI, including non-owner SR-22. Compare policy options in our Travelers insurance review.

Cons

- Poor customer service: Below-average for claims and customer service in multiple regions

- High rates for teens: Drivers under 25 pay more than with other companies

Free Auto Insurance Comparison

Enter your ZIP code below to view companies that have cheap auto insurance rates.

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

#8 – Nationwide: Cheapest With Bad Credit

Pros

- Cheap rates with bad credit: Charges much less than its competitors for drivers with bad credit scores

- Competitive low-mileage discounts: Save up to 20% when you drive less than 10,000 miles per year

- Pay-per-mile insurance: Reduce rates without tracking driving habits. Learn more in our Nationwide SmartMiles review.

Cons

- Poor customer service: Below-average for claims and customer service in multiple regions

- Not in every state: Nationwide is not available in AK, HI, LA, or MA

#9 – Allstate: Cheapest for Infrequent Drivers

Pros

- Great claims satisfaction: Top ten company in annual J.D. Power survey. Read more in our Allstate auto insurance review.

- Big low-mileage discounts: Save up to 30% when you drive less than 10,000 miles annually

- Pay-per-mile coverage: Allstate Milewise reduces rates without tracking driving habits

- Higher-mileage discounts: Milewise Unlimited helps drivers on the road more than 10,000 miles per year but less than 12,000 save money. Learn more in our Allstate Milewise review.

Cons

- Expensive: Charges over $100/mo for minimum coverage after a DUI

- Rate increases: Policyholders complain of higher rate increases at renewal than with other companies

#10 – Liberty Mutual: Cheapest With Discounts

Pros

- Big multi-policy discounts: Bundle home and auto to save $950/year

- Big low-mileage discounts: Save up to 30% when you drive less than 10,000 miles annually

- Biggest anti-theft discount: Get up to 35% off for installing additional safety features in your vehicle

- Usage-based discounts: Save up to 30% with RightTrack UBI

Cons

- Poor customer service: Below-average for claims and customer service in multiple regions

- Expensive: Most expensive auto insurance company after a DUI on this list with rates over $100/mo for minimum coverage. Compare rates now in our Liberty Mutual auto insurance review.

Free Auto Insurance Comparison

Enter your ZIP code below to view companies that have cheap auto insurance rates.

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Best Cheap Auto Insurance Companies After a DUI

DUI car insurance quotes vary for several reasons. Still, certain companies tend to charge higher rates for coverage than others.

Erie Insurance has the best insurance rates for a DUI on average, charging $60 monthly. The second best insurance rates for a DUI is State Farm, which costs $45 monthly on average for minimum coverage.

DUI Auto Insurance Rates Increase by Provider

| Insurance Company | Clean Record | DUI/DWI | Rate Increase |

|---|---|---|---|

| $87 | $152 | 69% | |

| $62 | $104 | 66% | |

| $47 | $72 | 49% | |

| $32 | $60 | 84% | |

| $96 | $178 | 80% | |

| $63 | $129 | 125% | |

| $56 | $75 | 33% | |

| $47 | 64.72 | 30% | |

| $61 | $93 | 48% |

| $53 | $112 | 109% |

Nationwide and Erie increase rates more than other companies on this list, but Erie is still the cheapest auto insurance company with a DUI. Keep reading to learn more about the best auto insurance companies for high-risk drivers.

How a DUI Impacts Auto Insurance Rates

On average, car insurance rates increase by 74% after a DUI. In comparison, a person with a speeding ticket pays about 24% more, and someone at fault in an accident could pay around 47% more for auto insurance.

Auto Insurance Monthly Rates by Driving Record

| Age & Gender | Speeding Ticket | At-Fault Accident | DUI/DWI |

|---|---|---|---|

| 16-Year-Old Male | $250 | $300 | $350 |

| 16-Year-Old Female | $240 | $290 | $340 |

| 20-Year-Old Male | $200 | $250 | $300 |

| 20-Year-Old Female | $190 | $240 | $290 |

| 30-Year-Old Male | $150 | $200 | $250 |

| 30-Year-Old Female | $140 | $190 | $240 |

| 40-Year-Old Male | $147 | $173 | $209 |

| 40-Year-Old Female | $147 | $173 | $209 |

| 50-Year-Old Male | $140 | $165 | $200 |

| 50-Year-Old Female | $135 | $160 | $195 |

| 60-Year-Old Male | $130 | $155 | $190 |

| 60-Year-Old Female | $125 | $150 | $185 |

A rate increase will be the most significant change to your car insurance after a DUI conviction. However, your auto insurance company may also drop your coverage, leaving you wondering how to get auto insurance with a DUI.

As a high-risk driver, you may need to consider non-standard auto insurance companies offering coverage to people with poor driving records. Unfortunately, you'll pay higher rates based on your status as a high-risk driver, but it’s important to find DUI auto insurance coverage before driving.Jeffrey Johnson Insurance Lawyer

Rate increases for people with a DUI vary from state to state. When looking for cheap car insurance with a DUI, it’s essential to compare rates from multiple companies based on where you live. Doing so will help you determine which company offers the best insurance for a DUI in your area.

Read More:

DUI Auto Insurance Rates by State

Where you live is one of the most significant factors that impact your auto insurance quotes for DUI drivers. We did some research and found the average monthly rate by state. We’ve also included which company is the cheapest in each state.

Auto Insurance Monthly Rates After a DUI by State

| State | Clean Driving Record | Rates After DUI | Rate Increase | Cheapest Company |

|---|---|---|---|---|

| Alabama | $42 | $84 | 77% | |

| Alaska | $32 | $64 | 99% | |

| Arizona | $94 | $157 | 93% | |

| Arkansas | $78 | $105 | 52% | |

| California | $85 | $119 | 40% | |

| Colorado | $35 | $72 | 37% | |

| Connecticut | $79 | $137 | 67% | |

| Delaware | $304 | $863 | 43% | |

| Florida | $75 | $155 | 36% | |

| Georgia | $58 | $75 | 30% | |

| Hawaii | $45 | $69 | 54% | MetLife |

| Idaho | $33 | $60 | 82% | |

| Illinois | $49 | $78 | 59% | |

| Indiana | $42 | $79 | 88% | |

| Iowa | $38 | $63 | 66% | |

| Kansas | $50 | $78 | 56% | |

| Kentucky | $55 | $109 | 99% | |

| Louisiana | $79 | $150 | 90% | Hanover |

| Maine | $29 | $56 | 92% | |

| Maryland | $132 | $270 | 34% | |

| Massachusetts | $43 | $56 | 36% | |

| Michigan | $104 | $133 | 43% | |

| Minnesota | $115 | $196 | 72% | |

| Mississippi | $74 | $102 | 97% | |

| Missouri | $27 | $46 | 83% | |

| Montana | $35 | $78 | 64% | |

| Nebraska | $68 | $91 | 39% | |

| Nevada | $48 | $93 | 62% | |

| New Hampshire | $44 | $77 | 75% | |

| New Jersey | $79 | $122 | 54% | MetLife |

| New Mexico | $47 | $70 | 50% | |

| New York | $92 | $179 | 95% | |

| North Carolina | $56 | $94 | 68% | |

| North Dakota | $48 | $86 | 80% | |

| Ohio | $45 | $81 | 81% | |

| Oklahoma | $55 | $100 | 82% | |

| Oregon | $66 | $126 | 91% | Hanover |

| Pennsylvania | $71 | $96 | 35% | |

| Rhode Island | $53 | $185 | 91% | |

| South Carolina | $60 | $107 | 78% | |

| South Dakota | $20 | $32 | 60% | |

| Tennessee | $57 | $79 | 30% | |

| Texas | $79 | $131 | 66% | |

| Utah | $34 | $62 | 72% | |

| Vermont | $35 | $70 | 81% | |

| Virginia | $59 | $160 | 57% | |

| Washington | $46 | $96 | 38% | |

| West Virginia | $53 | $84 | 59% | |

| Wisconsin | $41 | $72 | 75% | MetLife |

| Wyoming | $39 | $77 | 98% | |

The average car insurance rates vary for each state. Overall, State Farm has the cheapest auto insurance rates for DUI drivers in the United States. Michigan is the most expensive state for car insurance. DUIs/DWIs increase your rates to 199%

How Long a DUI Affects Auto Insurance Rates

Expect your rates to increase for three to five years after your DUI conviction.

The amount of time a DUI affects rates differs depending on driving history, insurance company, and location. For instance, in some states, like North Carolina, insurance companies can only look back on a driving record for three years. Other states, like Massachusetts, allow five years.Tim Bain Licensed Insurance Agent

You’ll need to research your state’s laws to understand better how long your DUI insurance rates will be high.

High-Risk Auto Insurance After a DUI

According to the Centers for Disease Control (CDC), 29 people in the United States die from alcohol-impaired driving per day. To fight against DUI offenses, car insurance companies issue higher rates to offset the risk of filed claims and to deter drivers from driving while intoxicated (DWI).

Insurance companies may label you a high-risk driver if you have multiple DUIs on your record or a DUI with other serious driving infractions. As a result, some companies refuse to offer high-risk auto insurance for DUI drivers.

High-risk car insurance for DUI drivers is more expensive and offers fewer options.

If you're convicted of a DUI 🚔, you might pay 74% more for car insurance 💰, according to https://t.co/27f1xf1ARb. Even with a DUI on your record, you can take control of your insurance options and search for better rates. Find out more here 👉: https://t.co/BN5jVydqXx pic.twitter.com/FKhuGNzHa0

— AutoInsurance.org (@AutoInsurance) June 13, 2023

Suppose you can’t find a company willing to offer you car insurance after a DUI. In that case, you can access your state’s Automobile Insurance Plan Service Office, which offers coverage for people who can’t find insurance anywhere else.

This coverage offers the minimum auto insurance required by your state. While your vehicle won’t be covered if you get in an accident, it’ll help you pay for the property or bodily damage you cause.

Difference Between SR-22 and FR-44 Auto Insurance

If you have a DUI and still maintain your car insurance policy, you’ll probably need SR-22 certification.

Some people know SR-22, FR-44, and SR-50 as DUI insurance. But it’s not insurance.

SR-22 is a certification that shows that you have the minimum auto insurance requirement.

FR-44 is limited to Florida and Virginia. It’s a certification that specifically targets DUI-convicted drivers and unlicensed drivers that have been convicted of DUI. Also, FR-44 requires double the minimum requirements.

SR-50 is only in Indiana. It works the same as SR-22 certification. And you’re required to have it if you want to reinstate your driving privileges.

Free Auto Insurance Comparison

Enter your ZIP code below to view companies that have cheap auto insurance rates.

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

How Auto Insurance Companies Check Driving Records

You might be wondering how auto insurance companies check driving records. Most companies request copies of people’s driving records before offering them a policy. Any DUIs, accidents, tickets, or violations will appear when a company requests a copy of your driving record.

Even if you maintain a policy with the same company following your conviction, your insurer will learn about your DUI, particularly if you file a claim. Even if you don’t, your insurance company will likely check your driving record every year.

You may also be required to get SR-22 auto insurance with your insurance company following your DUI conviction. If this happens, your company will increase your rates immediately or drop you as a policyholder.

However, you can still find affordable DUI insurance by shopping for quotes online.

How to Lower Auto Insurance Rates With a DUI on Your Record

If you have a DUI on your driving record, you could lower your rates by doing one or more of the following:

- Prove you’re a good driver. Many auto insurance companies offer usage-based programs that track your driving habits. You could enroll in usage-based car insurance and allow companies to monitor your acceleration, braking patterns, and other things.

- Compare quotes. Before committing to any company, compare DUI car insurance quotes from multiple companies to see which offers the cheapest insurance for a DUI. Read more about how to evaluate auto insurance quotes.

- Ask about discounts. A DUI/DWI doesn’t disqualify you from getting a discount. Auto insurance discounts can help you save up to 25% on your DUI auto insurance coverage. If you have a DUI on your record, you could get a discount for completing a safe driving course or having a vehicle with safety features.

Several factors determine whether affordable auto insurance for DUI drivers is available. But discounts can help you get better bargains.

How to Buy Cheap Auto Insurance After a DUI

While the consequences of a DUI are severe and long-lasting, there are ways you can save money on auto insurance after a DUI. Always remember to ask for discounts and consider shopping with pay-as-you-go-auto insurance companies that only track mileage.

Erie, State Farm, and Auto-Owners are the cheapest insurers overall, but compare rates from every company on our list to get the lowest premiums possible. If you avoid adding more infractions to your driving record, your rates will eventually decrease.

The easiest DUI insurance trick to getting cheap rates is comparing insurance companies online. Save money by comparing cheap DUI auto insurance quotes online right here.

Frequently Asked Questions

Which insurance is best after a DUI?

Erie insurance offers the cheapest auto insurance after a DUI.

What is the cheapest full coverage auto insurance after a DUI?

State Farm has the cheapest DUI insurance, averaging $112 monthly for full coverage auto insurance. You’ll also find affordable DUI auto insurance with Progressive, which costs $140 monthly on average. However, it’s vital to compare DUI car insurance quotes, since companies consider other factors when setting rates.

How much does a DUI raise your auto insurance rates?

Car insurance for DUI offenders increases by 74% on average, amounting to $209 monthly. However, DUI insurance rates vary based on several factors, including chosen company and driving characteristics.

How long does a DUI affect auto insurance?

Auto insurance rates after a DUI will remain high for 3-5 years depending on where you live.

Is there a trick to getting cheap auto insurance after a DUI?

Comparison shopping online is the best DUI insurance trick for getting cheap rates. Compare at least three auto insurance companies and ask about discounts.

How do insurance companies find out about your DUI?

Most insurers discover your DUI conviction by checking your driving record. So, not telling insurance about DUI won’t prevent rate increases since the company checks your record anyways.

What’s SR-22 auto insurance?

SR-22 auto insurance proves you have financial responsibility in the event of a car accident. Some states require people to file an SR-22 after getting a DUI. Many car insurance companies will file an SR-22 on their client’s behalf.

What is the difference between SR-22 and FR-44 auto insurance?

FR-44 insurance requires higher liability limits than SR-22 coverage.

Who has the cheapest SR-22 insurance after a DUI?

Progressive has the cheapest SR-22 car insurance after a DUI.

Does USAA offer FR-44 insurance?

Yes. You’ll pay about $108/mo for USAA auto insurance after a DUI, almost double the average for drivers with a clean record.

Can auto insurance companies deny a policy because of a DUI?

The short answer is yes. If a car insurance company believes you’re too risky to insure, they will deny your coverage request.

Will insurance cover a totaled car with a DUI?

Generally, your auto insurance will still pay out even after a DUI. However, it depends on the terms and conditions of your policy.

Can my auto insurance increase if I wasn’t in an accident but got a DUI?

Auto insurance rates for drivers with a DUI may still go up after a conviction. Your DUI suggests you’re a risk on the road due to poor judgment, even if you weren’t in an accident.

Are there specialized insurance companies that cater to drivers with a DUI?

Yes, there are insurance companies that specialize in providing coverage to high-risk drivers, including those with a DUI. These companies typically offer policies known as “non-standard” or “high-risk” insurance. While the premiums may still be higher than average, they may provide more affordable DUI auto insurance coverage options compared to traditional insurance companies.

How can I bounce back from a DUI?

The best way to bounce back from a DUI is to avoid traffic violations for at least three years.

Is it possible to remove a DUI conviction from my driving record and improve my insurance rates?

The process to removing a DUI conviction from your driving record varies by jurisdiction. In some cases, you may be able to expunge or seal the DUI conviction, effectively removing it from public view. However, insurance companies may still have access to certain records or databases that show your full driving history. It’s best to consult with a legal professional familiar with the laws in your area for guidance on record expungement.

Free Auto Insurance Comparison

Enter your ZIP code below to view companies that have cheap auto insurance rates.

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Brandon Frady

Licensed Insurance Agent

Brandon Frady has been a licensed insurance agent and insurance office manager since 2018. He has experience in ventures from retail to finance, working positions from cashier to management, but it wasn’t until Brandon started working in the insurance industry that he truly felt at home in his career. In his day-to-day interactions, he aims to live out his business philosophy in how he treats hi...

Licensed Insurance Agent

Editorial Guidelines: We are a free online resource for anyone interested in learning more about auto insurance. Our goal is to be an objective, third-party resource for everything auto insurance related. We update our site regularly, and all content is reviewed by auto insurance experts.