If someone hits my car, do I call my insurance or theirs?

You should always call your own insurance company after an accident, regardless of who you think is at fault. To ensure you're fully prepared for any scenario on the road, compare auto insurance rates to find the coverage that best suits your needs.

Read more

Table of Contents

Table of Contents

Insurance & Finance Analyst

Laura Adams is one of the nation’s leading finance, insurance, and small business authorities. As an award-winning author, spokesperson, and host of the top-rated Money Girl podcast since 2008, millions of readers and listeners benefit from her practical advice. Her mission is to empower consumers to live healthy and rich lives by planning for the future and making smart money decisions. She rec...

Laura D. Adams

Licensed Insurance Agent

Brandon Frady has been a licensed insurance agent and insurance office manager since 2018. He has experience in ventures from retail to finance, working positions from cashier to management, but it wasn’t until Brandon started working in the insurance industry that he truly felt at home in his career. In his day-to-day interactions, he aims to live out his business philosophy in how he treats hi...

Brandon Frady

Updated December 2024

If you’re in a car accident, you might feel disoriented and unsure about what steps to take next. Even if you believe you know who’s at fault, you may be uncertain about which insurance company to call. You may also wonder if it’s advisable to communicate with the other party’s insurance company. Additionally, if you were the one who caused the accident, you may question whether you should file a claim.

After exchanging details with the other driver and obtaining their insurance provider’s contact information, you might feel inclined to reach out to their insurer to initiate a claim. However, it’s crucial to resist this urge. Directly contacting the other party’s insurance company can detrimentally affect the compensation you may receive if someone hits your car. Instead, consider whether to file a claim with your insurance or theirs, as this decision significantly impacts the resolution process and who ultimately bears the financial responsibility if someone hits your car.

Instead, you need to report the accident to your own insurer. Read on to learn valuable information about what you are required to say when you have an accident and why you should not contact the other driver’s insurance company.

- Your auto insurance company represents you as the driver, and you are required to notify your insurance agent when you have an accident, regardless of who is at fault

- You should not contact the other driver’s insurance, as this may impair your ability to get compensation for damages from that insurer

- You want to work with your insurance adjuster on any claims issues rather than contacting the other driver’s company

Whose insurance should I call after an accident?

In the event of an accident, it’s essential to reach out to your insurance provider, irrespective of fault. Even if the other party is clearly responsible, refrain from reaching out to their insurer. For instance, if you were rear-ended, you should contact your insurance company.

When you contact the insurance company, you’ll need to provide basic information such as the date and time of the accident. However, do I have to call my insurance if someone hit me? Other essential details include the address of where the accident took place, the part of your car that was damaged, and where your vehicle was taken after the accident.

You should also be able to recount details that led to the accident and the driving conditions. Write down this info at the time of the accident so you can give it to your insurer:

- Police report number

- Names of passengers or witnesses

- Insurance policy information for other drivers

- Name of the other drivers involved

Your insurance company will need complete and accurate information to process your claim correctly.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

What should you do after a car accident?

When you sign up for a car insurance policy, you agree to pay premiums for coverage by the insurer if you file a claim. As the policyholder, you also agree to specific terms and conditions. You want to make sure you have a good understanding of your car insurance policy.

After an accident, the question of “whose insurance to call” often arises amidst the overwhelming number of terms and conditions listed in your policy. However, you can comply with most of these obligations by maintaining your vehicle and license and not taking additional risks.

Most insurance companies mandate that policyholders notify them if an incident occurs that might lead to a claim. When in an accident, do I call their insurance? No, you should contact your own insurance first.

Insurers usually provide a timeframe for customers to notify an agent of an incident. After an accident, I call my insurance. I need to notify my insurance if someone hits me as soon as I am reasonably able to do so.

Consequences for Not Reporting Accidents

Insurance companies take notification requirements seriously for several reasons. The primary purpose is to limit the number of fraudulent claims filed. Remember that even if you don’t think you need to file a claim, the other drive might file one, and your insurance company will be contacted.

If I file a claim with my insurance after an accident but fail to report it, my insurer could cancel my policy. Losing coverage means I might have to cover any claims out of my own pocket.

Failing to report an accident can lead to severe consequences, including the possibility of your insurer terminating your policy. This could leave you financially responsible for any claims, highlighting the critical nature of timely accident notification.Daniel Walker Insurance Agent

If you do not inform your insurance agent about the incident, the insurance company could deny any claims against you. This would make you personally responsible for any damages to third parties. So, do I have to tell my insurance if someone hits me? Yes, you must.

Failing to report an incident violates your insurance agreement, allowing the insurer to refuse to fulfill its obligations. This raises the question: should I use my insurance or theirs?

Protection by Providing Notification

Your first line of defense against a false claim or an unfavorable coverage determination is to notify your insurer of any incident.

If someone hits my car, do I need to contact my insurance? Indeed, there is a misconception among some individuals who fear that reporting incidents could lead to increased insurance rates. However, this belief is unfounded. In reality, failing to report an accident violates the terms and conditions of your insurance agreement, potentially resulting in policy cancellation. This omission could ultimately prove more costly, as you would be responsible for covering damages personally.

If your policy is not canceled, your claim may be denied, or you could be found at fault. If the claim is denied, you would have to pay for any damages. If you are found at fault, your rates can get raised.

After being rear-ended, you may wonder whether to contact your insurance or the other driver’s. In such cases, it’s typically wise to reach out to your own insurance company. They will likely assign an adjuster to assess the claim. Adjusters are skilled at gathering information advantageous to the insurer, aiming to minimize payouts.

During discussions, be mindful as your conversation might be recorded, and any statements could potentially work against your interests, affecting your ability to receive fair compensation for damages. Your insurance company’s adjuster will work on your behalf to make sure the other driver’s insurance covers the damages as required.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Getting Repairs Done Quickly

If the other driver’s insurance company is dragging its feet on paying your claim, you may not be able to use your vehicle for a while. You can avoid this situation by getting a full coverage policy through your insurer.

Under a full coverage policy, your insurer will pay for collision damages while awaiting the outcome of a final determination of who was at fault. If the other party is deemed responsible, your insurer will collect reimbursement for any payments made from the other driver’s insurer.

If you have an unsatisfactory experience in processing a claim with your current insurance, consider finding another carrier. Research the best companies for car insurance. Any existing claims will still need to be satisfied by your insurer at the time of the incident, so you may want to stay a customer until your claim is resolved.

Understanding Insurance Protocols After an Accident

When involved in a car accident, the immediate steps you take can significantly influence the outcome of your insurance claim. It’s crucial to understand that regardless of fault, your first call should be to your own insurance company. This protocol is in place to protect you. Your insurer can offer guidance, support, and begin the claims process. They’re also equipped to handle negotiations with the other party’s insurance, ensuring that your interests are represented. This approach simplifies the process, potentially speeds up the claims resolution, and helps avoid any miscommunication that could adversely affect your compensation.

Navigating Rear-End Collisions: Whose Insurance to Call

Rear-end collisions are among the most common types of traffic accidents, and they often come with clear fault determination. Even so, contacting your own insurance provider first remains the best course of action. This standard procedure allows your insurer to record the incident’s details and advise you on the next steps. They will typically handle communications with the other party’s insurer, including claims for damages or injuries. By letting your insurance company take the lead, you minimize the risk of jeopardizing your claim and ensure that professional negotiators are working on your behalf.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Exchange of Insurance Information: Dos and Don’ts

At the accident scene, exchanging insurance information with the other driver is a critical step. Ensure you collect their full name, contact information, insurance company name, policy number, and the vehicle’s license plate number. Avoid discussing fault or details of the incident during this exchange. Anything said can be misconstrued or used against you in the claims process. Instead, focus on gathering information and documenting the scene with photos. This documentation will be invaluable to your insurance company as they process your claim.

When to Consider Going Through the Other Driver’s Insurance

There are specific instances where dealing directly with the other driver’s insurance may seem straightforward, such as in clear cases of fault. However, initiating a claim through your insurance company is advisable even then. Your insurer can evaluate whether it’s in your best interest to file the claim through your policy or pursue the other driver’s insurance for damages. In scenarios where the other party is clearly at fault and admits liability, your insurer might decide to reclaim the deductible and repair costs from the other party’s insurance, a process known as subrogation. This approach ensures that you’re fully supported throughout the claims process and helps avoid potential pitfalls of navigating insurance claims independently.

Final Advice on Reporting Accidents

Who calls insurance after an accident? Following an accident, it’s crucial to reach out to your insurance provider promptly to inform an agent of the incident. Neglecting to report the occurrence may result in adverse outcomes, including potential policy cancellation or denial of claims. It’s essential to remember that it’s the policyholder who initiates contact with the insurance company after an accident.

It is never in your best interest to contact the other driver’s insurance company. You can also get your car repaired while awaiting a final determination of responsibility if you have a full coverage policy through your insurance company.

Frequently Asked Questions

If another driver hits my car, who should I call first – my insurance company or theirs?

In the event that someone hits your car, it’s generally recommended to contact your own insurance company first. Regardless of who is at fault, it is important to inform your insurance provider about the accident as soon as possible. They can guide you through the claims process and provide the necessary support, especially if “my car on call” or “my car was hit and their insurance won’t pay California.

Why should I call my own insurance company if the other driver caused the accident?

Calling your car insurance company is crucial for several reasons. They help protect your rights and ensure your claim is properly managed. They provide guidance on the steps to take and the information needed at the accident scene. Additionally, if the other driver is at fault, their insurance might not fully cover the damages, or they may be uninsured. In such cases, your policy might include uninsured or underinsured motorist coverage, which can help with your expenses. Insurance can find out about the accident, so it’s important to report it promptly.

What information should I gather when someone hits my car?

When involved in a car accident, it’s crucial to gather important information from the other driver and any witnesses. Here are the key details to collect:

- The other driver’s full name, contact information, and insurance details (if available).

- License plate number and vehicle make/model of the other car.

- Date, time, and location of the accident.

- Photos or videos of the accident scene, including damages to both vehicles.

- Contact information of any witnesses present.

- Police report number, if applicable.

What should I do if the other driver’s insurance company contacts me directly?

If the other driver’s insurance company calls you directly, it’s generally advisable to politely decline providing them with a detailed statement or discussing the accident in-depth. Instead, inform them that you will be reporting the incident to your own insurance company and that they should contact your insurance company for further information. Remember, your car insurance company is there to protect your interests and handle the claims process on your behalf. If you are rear-ended, whose insurance to call is your own insurance company first.

Will filing a claim with my insurance company affect my premium, even if I’m not at fault?

If someone hit me, filing a claim with my insurance company might or might not impact my premium, based on my specific policy and local insurance regulations. Typically, if I’m not at fault and the other driver’s insurance covers all expenses, my own rates may remain unchanged. However, it’s advisable to review my insurance policy or speak with my insurance agent to understand whether it is better to go through my insurance or theirs and how filing a claim could affect my premiums.

If someone rear-ends me, whose insurance do I call?

Always call your own insurance first after an accident. They will guide you on the next steps and, if necessary, deal with the other driver’s insurance on your behalf, especially if you have full coverage and someone hit you.

Do I need to contact my insurance if someone hits me?

It is crucial to notify your own insurance provider about the accident if someone hits you, as this safeguards your rights and starts the claims procedure if necessary. Remember to reach out to Direct Auto Insurance directly.

If someone hits my car, whose insurance do I call?

Initiate contact with your auto insurance company first. They can make the necessary auto insurance calls to the other driver’s insurance and handle the debut of negotiations for compensation directly.

If I get rear-ended, whose insurance do I call?

Contact your own insurance company after the accident. They will assist you in documenting the incident and provide advice on the necessary steps, including determining if you should file a claim.

Do I have to give my insurance information if someone hits me?

Yes, you should provide your insurance information to the other driver.

Related Articles

-

Dec 2024

Does auto insurance cover putting in the wrong fuel?

-

Mar 2025

Do you need auto insurance to be towed? (What You Should Know for 2026)

-

Jan 2025

How to Add Someone to My Auto Insurance for 1 Week in 2026 (5 Simple Steps)

-

Feb 2025

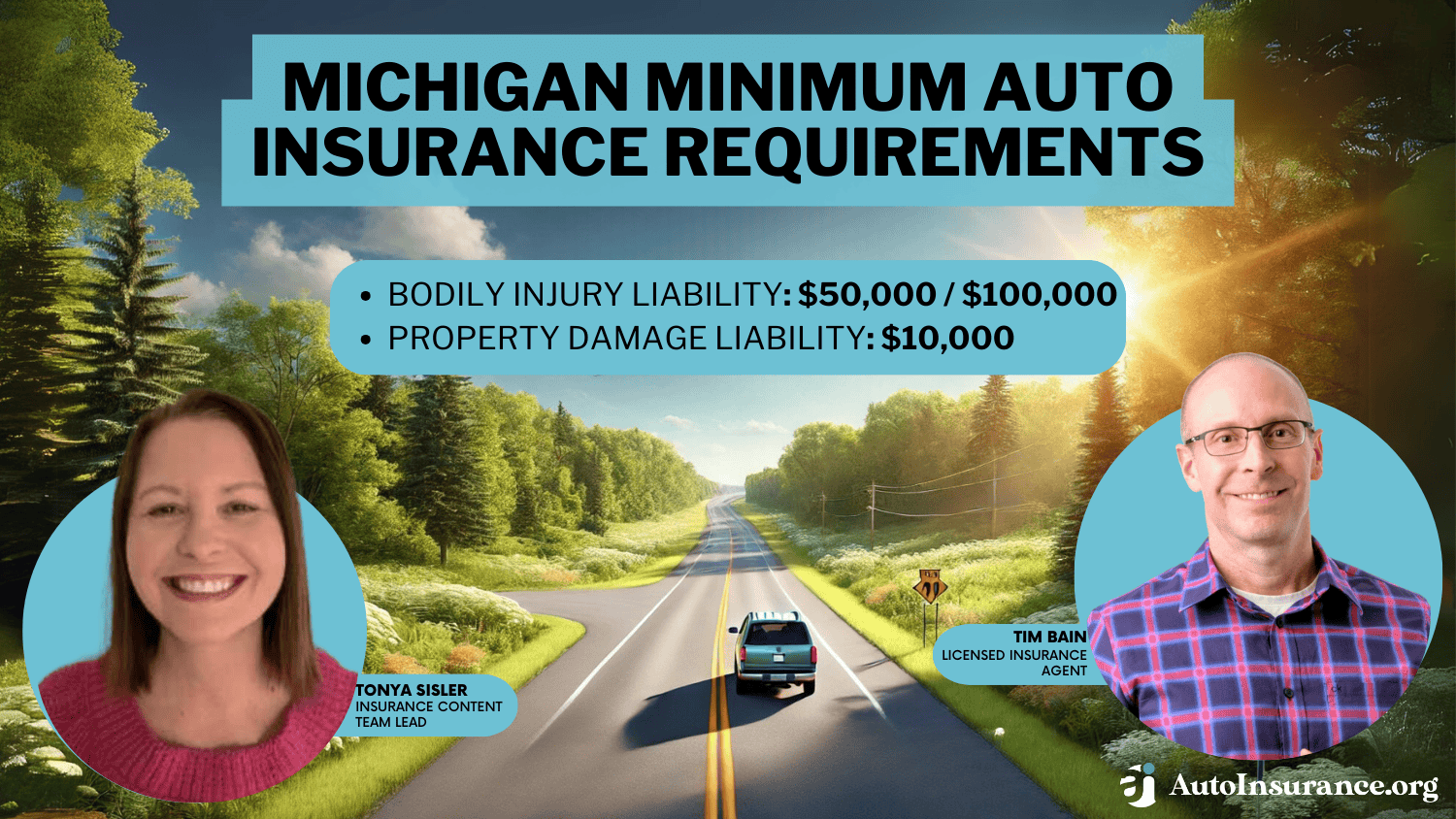

Michigan Minimum Auto Insurance Requirements in 2026 (Coverage You Need in MI)

-

Nov 2024

Rental Car Reimbursement Coverage in 2026 (Insurance Guide)

-

Mar 2025

Best Windshield Replacement Coverage in Oklahoma (Our Top 10 Picks for 2026 )

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.