Cheap Auto Insurance for Teens of Divorced Parents in 2026 (Top 9 Companies Ranked)

Explore cheap auto insurance for teens of divorced parents with Erie, USAA, and State Farm, starting at $136 per month. These insurers have 50-50 custody auto insurance, minimum coverage, safe driver, and good student discounts. Compare plans for divorced families to optimize affordability and coverage.

Read more

Find the Lowest Car Insurance Rates Today

Quote’s drivers have found rates as low as $42/month in the last few days!

Table of Contents

Table of Contents

Insurance and Finance Writer

Laura Gunn is a former teacher who uses her passion for writing and learning to help others make the best decisions regarding finance and insurance. After stepping away from the classroom, Laura used her skills to write across many different industries including insurance, finance, real estate, home improvement, and healthcare. Her experience in various industries has helped develop both her ...

Laura Gunn

Licensed Insurance Agent

Brandon Frady has been a licensed insurance agent and insurance office manager since 2018. He has experience in ventures from retail to finance, working positions from cashier to management, but it wasn’t until Brandon started working in the insurance industry that he truly felt at home in his career. In his day-to-day interactions, he aims to live out his business philosophy in how he treats hi...

Brandon Frady

Updated April 2025

1,883 reviews

1,883 reviewsCompany Facts

Teens After Divorce Min. Coverage

A.M. Best Rating

Complaint Level

Pros & Cons

1,883 reviews 6,590 reviews

6,590 reviewsCompany Facts

Teens After Divorce Min. Coverage

A.M. Best

Complaint Level

Pros & Cons

6,590 reviews 18,157 reviews

18,157 reviewsCompany Facts

Teens After Divorce Min. Coverage

A.M. Best

Complaint Level

Pros & Cons

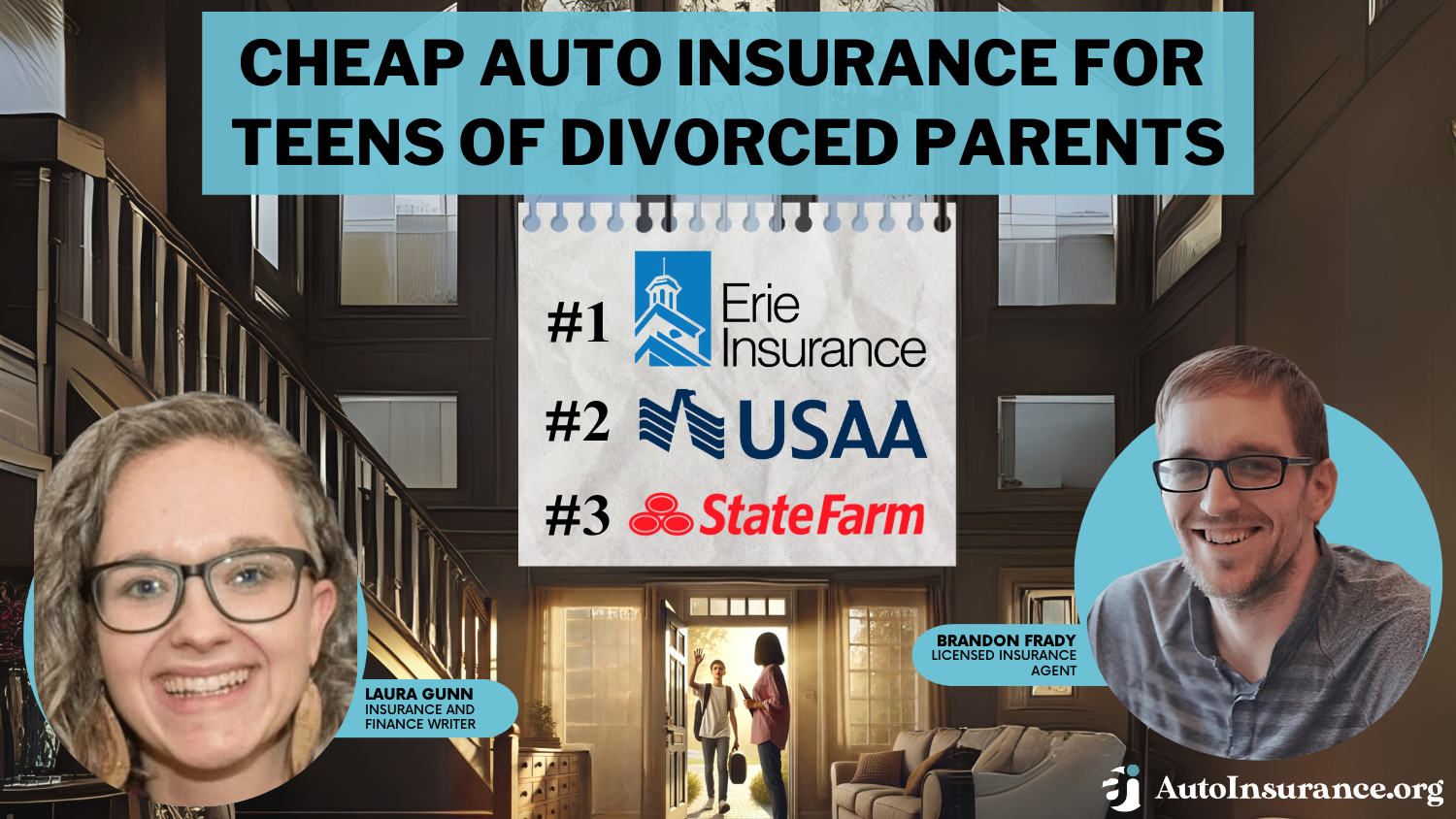

18,157 reviewsErie, USAA, and State Farm are the top picks for cheap auto insurance for teens of divorced parents, with rates starting as low as $136 per month.

These providers offer competitive pricing and comprehensive coverage options, including comprehensive auto insurance tailored for families with shared custody arrangements, such as 50-50 custody auto insurance.

Our Top 9 Company Picks: Cheap Auto Insurance for Teens of Divorced Parents

| Company | Rank | Monthly Rates | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | $136 | A+ | Customer Savings | Erie | |

| #2 | $146 | A++ | Military Families | USAA | |

| #3 | $208 | A++ | Low Rates | State Farm | |

| #4 | $279 | A+ | Deductible Savings | Nationwide | |

| #5 | $296 | A | Young Volunteers | American Family | |

| #6 | $371 | A+ | UBI Insurance | Allstate | |

| #7 | $452 | A | Family Plans | Farmers | |

| #8 | $464 | A | Add-on Options | Liberty Mutual | |

| #9 | $467 | A+ | Budgeting Tools | Progressive |

They offer discounts for safe driving and good grades, making them top choices for budget-savvy consumers. Compare these providers to find the best deal and benefits for your teen.

You can also enter your ZIP code to compare quotes from multiple companies and find the best auto insurance for teens of divorced parents.

- Affordable plans starting at $136 per month cater to teens of divorced parents

- Erie is the top pick, offering the best rates and comprehensive coverage

- Policies include 50-50 custody options and discounts for good grades

#1 – Erie Insurance: Top Overall Pick

Pros

- Youth Driver Discounts: Erie offers a youthful driver discount, though you’ll need to speak with a representative to qualify.

- Excellent Customer Service: Erie prioritizes its policyholders, achieving higher customer satisfaction than many competitors. Compare Erie’s rates with top competitors in our review of Erie auto insurance.

- YourTurn: YourTurn is Erie’s UBI program that tracks driving behaviors like speeding and hard braking. Rather than offering a discount, YourTurn rewards safe drivers with cash rewards.

Cons

- No Online Quotes: Erie’s website lacks some of the online tools that bigger companies have. If you’re interested in an Erie policy, you’ll need to speak with a representative.

- Low Availability: Erie is a smaller insurance company and currently only sells coverage in 12 states.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#2 – USAA: Best for Military Families

Pros

- Safe Driving Discounts: You’ll find savings for being a safe driver among USAA’s 14 car insurance discounts.

- Affordable Rates: USAA is almost always the cheapest option for car insurance, no matter where you live. To learn more about why USAA’s rates are so cheap, read our USAA auto insurance review.

- SafePilot: USAA’s UBI program SafePilot offers a maximum savings of 30% if you consistently practice safe driving behaviors.

Cons

- Eligibility Requirements: Teens need at least one parent to be either active or retired military to qualify for USAA membership.

- Some Coverage Options Lacking: USAA doesn’t have a few popular policy add-ons, like gap insurance.

#3 – State Farm: Top Pick Overall

Pros

- Academic Excellence Offers: State Farm provides several student discounts, including a popular 25% good student discount for maintaining high grades.

- Steer Clear Program: The Steer Clear program helps young drivers improve their skills by giving them helpful feedback. Earn a discount of up to 15% by completing the program.

- Drive Safe and Save: State Farm’s Drive Safe and Save is a usage-based insurance program that monitors driving behavior. Learn about potential savings in our State Farm auto insurance review.

Cons

- Limited Online Options: Claims can be started in the app, but buying a policy and other inquiries require phone communication, as there’s no live chat option.

- Add-Ons Lacking: State Farm has everything you need for standard coverage, but it lacks some popular add-on choices. For example, you can’t add accident forgiveness or gap insurance to your policy.

#4 – Nationwide: Best Vanishing Deductible for Safe Drivers

Pros

- SmartRide: Get an instant 10% discount on your insurance with Nationwide’s SmartRide UBI program. After a 4-6 month evaluation, your discount could increase to up to 40%.

- Vanishing Deductible: Sign up for the vanishing deductible program to lower your deductible by $100 every year you remain claims-free, up to $500.

- Add-On Options: Nationwide offers several valuable add-ons, including gap insurance, car key replacement, and pet insurance.

Cons

- Limited Local Agents: Nationwide has fewer local representatives than some of its competitors, making it more challenging to get face-to-face help in some areas.

- Not Available Everywhere: Despite its name, Nationwide is not available in every state. Check our Nationwide auto insurance review to see if you can buy a Nationwide policy in your state.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#5 – American Family: Best for Young Volunteers

Pros

- KnowYourDrive: KnowYourDrive is a telematics program that drivers of all ages are eligible to enroll in. You can save up to 20% with KnowYourDrive.

- Teen Safe Driver Program: The teen safe driver program is a UBI initiative for teens, offering safe driving discounts and personalized improvement tips.

- Good Student Discounts: American Family provides discounts for young students who maintain a good GPA, volunteer for at least 40 hours yearly, or pass a defensive driving class.

Cons

- Limited Availability: American Family sells insurance in just 19 states. Learn more about American Family’s availability in our American Family auto insurance review.

- Higher Charges: While it doesn’t have outrageously high rates, you’ll likely find lower prices with companies other than American Family.

#6 – Allstate: Best UBI Savings

Pros

- Drivewise: Safe drivers can save up to 40% with Allstate’s Drivewise UBI program. Their Milewise program, detailed in our Allstate auto insurance review, is also available in select states.

- Coverage Options: Allstate offers a wide variety of coverage options to help you personalize your policy, including accident forgiveness and new car replacement.

- Savings Options: Allstate offers multiple savings for young drivers, including discounts for good grades, accident-free records, and opting for paperless documents.

Cons

- Higher Rates: Allstate provides extensive coverage but generally charges higher rates. While young drivers may find affordable options, it’s typically more expensive for older drivers.

- Mixed Reviews: Many Allstate customers report feeling unsatisfied with their insurance experience, especially when it comes to customer service.

#7 – Farmers Insurance: Best Family Plans

Pros

- Extensive Network of Local Agents: Insurance can be confusing, especially for teens getting coverage for the first time. Farmers representatives are readily available in person or over the phone to help.

- Ample Discounts: Farmers offers a whopping 23 discounts to help drivers save, several of which are meant for teens. Explore your discount options in our Farmers auto insurance review.

- Signal App: Enroll in Farmers’ telematics program by downloading the Signal app. Driving safely while using the Signal app can save you up to 30% on your coverage.

Cons

- No Policies in Florida: Farmers announced in 2023 that it would no longer sell new policies in Florida.

- Lacking Online Options: While most major car insurance companies are moving towards digital policy management, Farmers offers fewer options to manage your coverage online.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#8 – Liberty Mutual: Best for Add-on Options

Pros

- RightTrack: Save up to 30% on your coverage by enrolling in RightTrack, Liberty Mutual’s telematics insurance program.

- Discount Opportunities: Liberty Mutual offers several ways for young drivers to keep their rates as low as possible, plus several other discount options.

- Diverse Coverage Options: Adding coverage raises your rates, but Liberty Mutual offers many options for those with flexible budgets. Read our review of Liberty Mutual to explore your add-on options.

Cons

- Rates Can Be High: Liberty Mutual’s rates are usually close to the national average. It has affordable rates for younger drivers eligible for discounts, but older drivers might see less competitive rates.

- Below Average Claims Satisfaction: Liberty Mutual struggles with its customer service, claims satisfaction, and overall trustworthiness ratings.

#9 – Progressive: Best for Teens on a Budget

![]()

Pros

- Name Your Price Tool: Teen auto insurance can be expensive, but Progressive’s Name Your Price tool lets you enter your budget to view available coverage options.

- SnapShot: Agree to have your driving habits tracked with Progressive’s Snapshot program to save on your insurance. The average driver saves $156 annually after signing up for Snapshot.

- Teen Driver Discounts: Progressive offers discounts for young drivers, including a specific one for policies with drivers under 18. For discount information, check out our Progressive auto insurance review.

Cons

- SnapShot Increase Rates: Unlike most UBI programs, Snapshot can increase your rates if you don’t consistently practice safe driving habits.

- Mixed Ratings: Despite being one of the largest insurance providers in the country, Progressive struggles with its customer service ratings.

Auto Insurance for Teens of Divorced Parents Rates

Teenage auto insurance rates are almost always higher than coverage for older adults, but some companies offer better prices than others.

Insurance companies view teens as high-risk due to reckless behavior. Taking a defensive driving course can reduce these risks.Brandon Frady Licensed Insurance Producer

Check below to see the average minimum insurance cost for teen drivers from companies with the cheapest teen auto insurance.

Minimum Coverage Auto Insurance Monthly Rates for Teens of Divorced Parents

| Insurance Company | 16-Year-Old Male | 16-Year-Old Female | 18-Year-Old Male | 18-Year-Old Female |

|---|---|---|---|---|

| $371 | $338 | $318 | $275 | |

| $296 | $230 | $253 | $187 | |

| $136 | $121 | $116 | $99 | |

| $452 | $452 | $387 | $368 | |

| $464 | $404 | $398 | $329 | |

| $279 | $230 | $239 | $187 | |

| $467 | $440 | $400 | $358 | |

| $208 | $177 | $178 | $144 | |

| $146 | $137 | $125 | $111 |

Minimum insurance is your cheapest option for coverage, but it’s not the best protection. Check the average full coverage rates below to see if you might have room in your budget for more protection.

Full Coverage Auto Insurance Monthly Rates for Teens of Divorced Parents

| Insurance Company | 16-Year-Old Male | 16-Year-Old Female | 18-Year-Old Male | 18-Year-Old Female |

|---|---|---|---|---|

| $910 | $868 | $740 | $640 | |

| $726 | $590 | $591 | $435 | |

| $332 | $311 | $270 | $229 | |

| $1,103 | $1,156 | $897 | $852 | |

| $1,120 | $1,031 | $893 | $745 | |

| $679 | $586 | $552 | $432 | |

| $1,161 | $1,143 | $944 | $843 | |

| $498 | $443 | $405 | $327 | |

| $356 | $349 | $289 | $257 |

Teen auto insurance rates can be up to four times as expensive as what older adults pay, but a guardian or parent can help them save up to 50% by adding them to an existing policy.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

50-50 Custody Auto Insurance for a Child of Divorced Parents

In most cases, the parents of a teenage driver add the child to their auto insurance coverage plans. If you are divorced, your teenager’s auto insurance coverage depends on you and your ex-spouse’s custody arrangement. Typically, if you are the parent with primary custody, you will add the teen to your car insurance plan.

>However, if you share joint custody of your child, you and your former spouse have more options, including 50-50 custody auto insurance for your teen. In joint custody arrangements, both parents usually add their child to their car insurance policies, especially if the teenage driver uses a car at both residencies. After your child turns 18, custody rules will no longer apply.

Auto Insurance Rates for Teenage Drivers

Teenage drivers have some of the most expensive auto insurance rates among motorists. Their auto insurance rates are higher than average due to the heightened risk associated with their age. To illustrate, the National Highway and Traffic Safety Administration (NHTSA) explains that teenagers have a higher rate of fatal accidents because of their lack of experience operating a motorized vehicle.

While adding a teenage driver to your plan, auto insurance companies will typically apply a surcharge to your insurance rates. The surcharge protects your insurance company from any major losses caused by your child.

If your teenage driver causes an accident or gets a ticket, the surcharge is likely to be much higher. Sometimes, this additional cost can remain on your bill for as long as five years. The high cost of insuring a teenager will likely make 50-50 car insurance policies appealing for parents who share custody.

Keeping Your Teenage Driver Safe

You and your ex-spouse may want to share relevant fatality statistics with your teen and establish ground rules to ensure that your child prioritizes safety while driving.

Auto insurance laws reinforce the need to follow driving rules such as always wearing a seatbelt, observing speed limits, and avoiding impaired driving. The NHTSA advises clear consequences for any rule violations.

Auto Insurance Requirements for Teenage Drivers

Even if your child does not have their own car yet, your teen must still be covered under insurance if they are driving. There are some general steps that you should take to ensure that your teen has the proper auto insurance coverage.

You should first contact your auto insurance agent to notify them of an additional driver in your household. Your auto insurance company will then request updated information concerning your teen’s driving status.

Definition Card: Cheap Auto Insurance for Teens of Divorced Parents")

If your child ends up purchasing a car in their own name, the auto insurance company must receive notification about this change as soon as possible. If not, your child may not have coverage. If your child is in an accident without coverage, you will likely spend an enormous amount of money and may need to hire a lawyer to mitigate the consequences.

Insurance companies know the requirements in your state, which is why they ask for your ZIP code first when getting a quote. An uninsured accident may also damage your teen’s driving record, leading to higher auto insurance rates for several years. Auto insurance for teens after an accident is almost always expensive.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Teen Auto Insurance Options

If avoidable, teen drivers should not be listed as a policyholder on their own policy. In fact, most auto insurance companies will not agree to provide this type of coverage for a teen driver because of their notorious high risk.

Even if your teen can get auto insurance as a policyholder, they will likely be unable to pay for insurance rates by themselves.

Adding Multiple Vehicles to Your Policy

It is generally cheaper to add a second vehicle to your insurance policy. Some auto insurance companies will offer a discount if you have multiple cars insured under the same insurance plan. If you purchase a new vehicle in your name for your child, the price per vehicle for your auto coverage will likely drop.

In short, listing all vehicles in your household under the same policy is financially wise since separate auto insurance policies cost more without a discount.

Good Student Discounts for Teen Drivers

Most auto insurance companies will offer a good student discount. Upon providing proof that your teenager has an exceptionally high grade point average, most insurance companies will offer a student discount in recognition of their responsible behavior.

As a feature writer, I discovered Erie's 50-50 custody coverage and good student discount provide significant savings for families.Tonya Sisler Insurance Content Team Lead

Teen drivers who earn good grades are generally less likely to engage in reckless behavior while on the road.

Top Auto Insurance Choices for Teens of Divorced Parents

If you want specific cheap auto insurance for teens of divorced parents who are looking for good joint custody insurance, the best comprehensive auto insurance companies are Erie, USAA, and State Farm. They offer competitive rates starting at $136 per month, along with comprehensive coverage options such as 50-50 custody auto insurance.

In addition, these companies offer safe driving discounts and good student discounts that match well to the unique needs of divorced families trying to maximize both cost and coverage for their teenage drivers.

Enter your ZIP code into our free quote comparison tool to find the cheapest rates for teens of divorced parents.

Frequently Asked Questions

What is the best approach for title and registration when divorced parents buy a car for their child?

Title and registration of the vehicle, including which parent’s address will be used for registration. This decision may have implications for your insurance premiums and also for who pays tax on the vehicle. Some parents decide to co-title the vehicle to make things easier.

Is a non-custodial parent responsible for car insurance if the child primarily resides with the other parent?

While the primary custodial parent typically handles day-to-day expenses, including car insurance, non-custodial parents may be required to contribute financially, depending on the terms set by the court or agreed upon in the custody arrangement.

You can find the cheapest insurance coverage tailored to your needs by entering your ZIP code.

Are there specific discounts available on car insurance for a child of divorced parents?

While there aren’t specific discounts for children of divorced parents, the child might qualify for general discounts offered to families, such as good student and safe driving bonuses, primarily if the parent uses one of the best auto insurance companies for multiple vehicles.

Can car insurance for kids include coverage for driving to school or extracurricular activities?

Yes, coverage for driving kids to school and extracurriculars can be included on young driver car insurance. But details of what’s included can vary by provider, so check with the insurer.

What factors should divorced parents consider when choosing car insurance for their teen drivers?

When selecting car insurance for divorced parents, it’s important to consider which parent’s address will be used as the teen driver’s primary residence, the type of coverage needed based on the teen’s driving habits, and how costs can be effectively managed between both parents.

How does car insurance work with divorced parents if one lives in a different state than the teen driver?

If one divorced parent lives in another state, the teen should be insured according to the minimum auto insurance requirements by state where they live. The visiting parent should be added as an additional insured. Constantly update the insurer on the teen’s living and driving locations.

Does the non-custodial parent have to pay for car insurance if the teen lives primarily with the custodial parent?

If the teen driver resides predominantly with the custodial parent, then the non-custodial parent usually does not have to cover the teen’s car insurance directly. But support agreements might involve paying a portion of large expenses, such as car insurance.

Do divorced parents need separate auto insurance policies for their children?

In general, if your child has a driver’s license and drives a car registered in their name, each parent needs to have an auto insurance policy. The best approach is to check with your insurance company and find out what is needed and available in your case.

Can “divorced parents car insurance for a child” impact the child’s future insurance rates?

If a child has an accident or multiple tickets, it could affect their future insurance rates. Maintaining a clean record can secure better rates, and using where to compare auto insurance rates can help find competitive options.

Can a child be covered under both parents’ auto insurance policies?

In some circumstances, children may be covered under both parents’ policies provided they spend equal time with each parent and both parents have valid auto insurance coverage. That said, it can differ depending on the insurance company, so it’s wise to confirm with your actual insurer.

Are there any discounts available for auto insurance when children of divorced parents are involved?

How does auto insurance work if the child primarily resides with one parent?

Does a parent or guardian have to put a teen driver on their policy?

Does having divorced parents affect car insurance rates?

How does separate car insurance for a teenager impact the insurance claims process?

Related Articles

-

Mar 2025

Cheap Auto Insurance for Drivers Over 80 in 2026 (Top 8 Companies Ranked)

-

Jun 2026

Nationwide SmartRide App Review (2026)

-

Jul 2026

10 Auto Insurance Companies With the Best Customer Service in 2026

-

Jul 2026

Government Assistance Programs for Low-Income Drivers in 2026 (Get Help Here!)

-

May 2025

Cheap Auto Insurance for Families With Multiple Drivers in 2026 (Save With These 8 Companies!)

-

Jun 2025

10 Best Auto Insurance Companies That Use LexisNexis in 2026

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.