10 Companies With the Cheapest Teen Auto Insurance in 2026

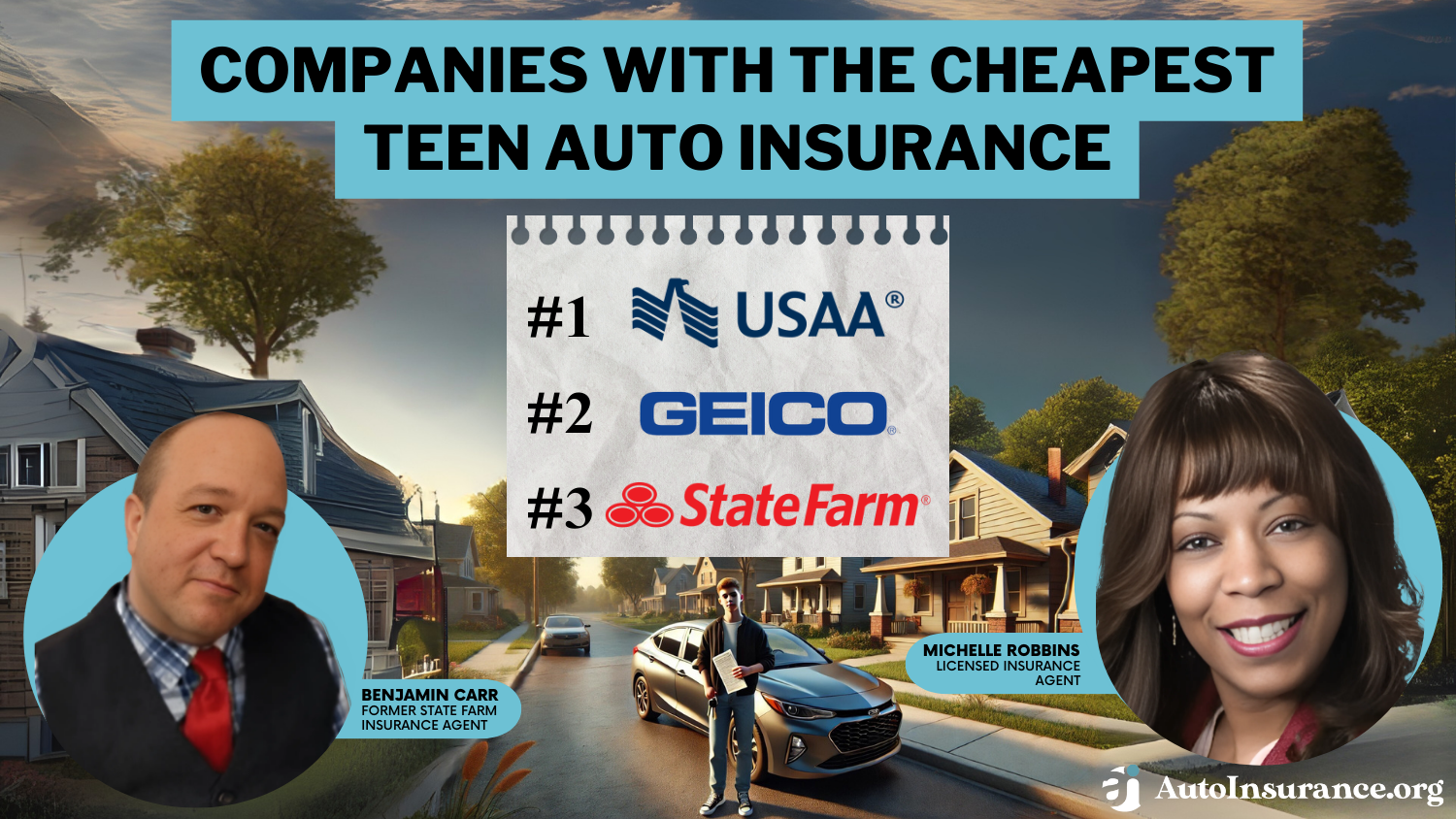

USAA, Geico, and State Farm are the companies with the cheapest auto insurance for teen drivers. Cheap teen car insurance starts at $146 per month with USAA, and our top picks help you save through special discounts, new driver training, and UBI programs that result in cheap car insurance for teenage drivers.

Read more

Find the Lowest Car Insurance Rates Today

Quote’s drivers have found rates as low as $42/month in the last few days!

Table of Contents

Table of Contents

Former State Farm Insurance Agent

Benjamin Carr worked as a licensed insurance agent at State Farm and Tennant Special Risk. He sold various lines of coverage and informed his clients about their life, health, property/casualty insurance needs. Assessing risks and helping people find the best coverage to suit their needs is a passion of his. He appreciates that insurance was designed to protect people, particularly during times...

Benjamin Carr

Licensed Insurance Agent

Michelle Robbins has been a licensed insurance agent for over 13 years. Her career began in the real estate industry, supporting local realtors with Title Insurance. After several years, Michelle shifted to real estate home warranty insurance, where she managed a territory of over 100 miles of real estate professionals. Later, Agent Robbins obtained more licensing and experience serving families a...

Michelle Robbins

Updated August 2025

6,590 reviewsCompany Facts

Min. Coverage for Teens

A.M. Best

Complaint Level

Pros & Cons

6,590 reviews 19,116 reviews

19,116 reviewsCompany Facts

Min. Coverage for Teens

A.M. Best

Complaint Level

Pros & Cons

19,116 reviews 18,157 reviews

18,157 reviewsCompany Facts

Min. Coverage for Teens

A.M. Best

Complaint Level

Pros & Cons

18,157 reviewsThe companies with the cheapest teen auto insurance are USAA, Geico, and State Farm. These insurers offer multiple discounts for teens to take advantage of and helpful training programs.

Our Top 10 Picks: Companies With the Cheapest Teen Auto Insurance

| Company | Rank | Monthly Rates | Good Student | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | $146 | 10% | Military Families | USAA | |

| #2 | $178 | 15% | Usage-Based | Geico | |

| #3 | $208 | 35% | Safe Drivers | State Farm | |

| #4 | $269 | 14% | Roadside Assistance | AAA |

| #5 | $279 | 18% | UBI Savings | Nationwide | |

| #6 | $296 | 20% | Driver Support | American Family | |

| #7 | $371 | 22% | Low Mileage | Allstate | |

| #8 | $452 | 15% | Discount Selection | Farmers | |

| #9 | $467 | 10% | Online Tools | Progressive | |

| #10 | $517 | 8% | Unique Coverage | Travelers |

USAA offers the cheapest car insurance for teen drivers at $146 per month, but only military families are eligible.

If that doesn’t apply to you, Geico and State Farm offer affordable rates and excellent auto insurance discounts for teens.

- Teens pay double or more for car insurance than older adults

- Most companies offer young driver discounts to help teens save

- USAA and Geico are the companies with the cheapest auto insurance for teens

Learn more about the companies with the cheapest teen auto insurance below. Then, enter your ZIP code into our free comparison tool above to see personalized auto insurance quotes.

The Cost of Auto Insurance for Teens

In either case, people generally encounter higher insurance rates until they enter their 20s. Age is one of the most important factors for car insurance — drivers under 25 will pay more for insurance the younger they are. Check the table below to see the minimum insurance costs for teens.

Teen Auto Insurance Monthly Rates by Age & Gender

| Insurance Company | Age: 16 Male | Age: 16 Female | Age: 17 Male | Age: 17 Female | Age: 18 Male | Age: 18 Female | Age: 19 Male | Age: 19 Female |

|---|---|---|---|---|---|---|---|---|

| $269 | $246 | $250 | $225 | $231 | $200 | $213 | $185 |

| $371 | $338 | $345 | $307 | $318 | $275 | $290 | $245 | |

| $296 | $230 | $275 | $209 | $253 | $187 | $232 | $168 | |

| $452 | $452 | $420 | $410 | $387 | $368 | $354 | $330 | |

| $178 | $163 | $165 | $148 | $153 | $132 | $142 | $117 | |

| $279 | $230 | $259 | $209 | $239 | $187 | $219 | $168 | |

| $467 | $440 | $433 | $401 | $400 | $358 | $368 | $319 | |

| $208 | $177 | $193 | $161 | $178 | $144 | $163 | $128 | |

| $517 | $392 | $480 | $355 | $443 | $319 | $407 | $286 | |

| $146 | $137 | $136 | $124 | $125 | $111 | $115 | $100 |

How much insurance is for a 16-year-old? USAA and Geico are the cheapest companies, starting at $137 monthly for minimum coverage, which is half the cost of the competition. You can compare rates to find cheap auto insurance for 16-year-olds.

Minimum insurance is your cheapest option for coverage, but it doesn’t offer your car very much protection. If you have some room in your budget, you should consider full coverage. Check below to see how much more full coverage costs.

You might notice that insurance for a 16-year-old is substantially higher than for even slightly older drivers. Although car insurance for 18-year-olds is cheaper, it’s incredibly high compared to older adults.

Understanding Auto Insurance Costs For Older Teens

What about the cost of auto insurance for a 17-year-old? These new drivers are not only more likely to get into an accident, but car insurance companies can’t look at their driving records to get an idea of how safe they are because they have no history.

Teens pay more for insurance due to their lack of driving experience. Teens are more likely to cause accidents or drive recklessly than older drivers.Heidi Mertlich Licensed Insurance Agent

If you’re looking for cheap car insurance for new drivers under 21, make sure to check for discounts. Since many 18- and 19-year-olds are either considering college or are already attending, many car insurance companies offer school discounts, including USAA and Geico.

Most states consider teens legal adults when they turn 18, which means they can buy insurance without a parent or guardian’s signature. However, young drivers won’t see significantly lower rates until around 25. Use this guide to find cheap auto insurance for drivers under 25.

However, age isn’t the only factor that determines your rates. Insurance companies also look at gender, location, driving history, and the make and model of your car. So, when you’re trying to figure out how much car insurance is for an 18-year-old per month, remember that your age isn’t the only thing that defines you.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Why Teen Auto Insurance Quotes Are So High

Auto insurance quotes for teens are high for one simple reason — risk. Car insurance companies want to insure the least risky people possible, and teen drivers are more likely to be involved in incidents than nearly every other demographic.

Do teens need auto insurance if they have a license but no car? Yes. Driving anyone’s vehicle presents a risk to teens that insurance companies don’t ignore. Since you are statistically more likely to get into an accident when you’re younger, you’ll be charged more for your insurance. To get an idea of why teen car insurance is so high, consider the following statistics:

- Car accidents are among the leading causes of death for young adults aged 15 to 20.

- Male teen drivers are twice as likely to die in a car accident as females.

- Having teen passengers increases the likelihood that a teen driver will cause an accident.

- Sixteen-year-old drivers are three times more likely to get into an accident than 19-year-olds due to the difference in their driving experience.

The good news is that your rates won’t stay high forever. Your rates will drop as you age as long as you keep your driving record clear.

Adding a Teen to Auto Insurance

Not only can a parent or guardian add a teen to their policy, but it’s also the best way to find affordable insurance for teenage drivers. Adding a young person to an existing policy can help teen drivers save up to 45% on auto insurance.

The good news is that adding a teen driver to your policy is usually simple. Most companies allow you to quickly add new drivers and vehicles to your policy online. Follow these tips for adding a driver to auto insurance.

Adding a teen driver to your car insurance policy is a simple process. If you already have a policy, adding a teen is as easy as calling an insurance representative. Once a new driver is added to your policy, your representative will check for new discounts that might apply.

You should add any teen with a new license to your policy if they’ll be driving a family car. Adding a teen driver to your insurance won’t raise your rates by too much and will ensure your vehicle is covered no matter who is driving. Teen driver insurance will cost more if they own a car, but it’ll still be cheaper than buying an individual policy.

When Teens Need Their Own Auto Insurance

Teens may wonder if they should get their own insurance, while a parent or guardian may ask if their child is covered by their auto insurance. While it’s more affordable for a teen to join a parent or guardian’s policy, there are times when buying their own insurance is necessary.

However, a minor usually can’t buy car insurance without a parent or guardian’s signature. The only exception to this is teens who have been emancipated by the court and are therefore able to make their own legal decisions.

Since minors can’t legally enter into contracts, insurance companies won’t sell an auto policy to anyone under age.Jeffrey Johnson Insurance Lawyer

In general, it’s cheaper for teens to join a parent’s or guardian’s policy. There are only a few occasions when teens should consider their own plans: when they are the only car owners in the household, or if other adults in the home have high-risk auto insurance, and joining their policy would cost more.

Unless any of these apply to you, joining a parent’s or guardian’s policy is the best way to find the cheapest car insurance for teens.

More Ways Teens Can Save Money on Auto Insurance

Although teen car insurance quotes are always higher, there are plenty of ways to save on your monthly rates. For example, usage-based auto insurance plans monitor your driving — as long as you practice safe habits, you’ll earn lower rates. If you don’t want your insurance company to track you, try the following to get cheap car insurance for teens:

- Take a Driving Class: Most major insurance companies offer a discount for teens who take approved driving courses, such as a defensive driving discount. As a bonus, teens can learn valuable driving skills.

- Keep a Clean Record: A clean driving record will save you money. Traffic incidents like speeding tickets or car accidents on your driving record can increase your rates.

- Increase Your Deductible: You can lower your monthly payment by increasing your deductible if you can afford to pay more before your insurance kicks in.

- Maintain Good Grades: There are auto insurance discounts for good students, so one of the best ways to save money on insurance for teens is to maintain a GPA of at least 3.0.

Good student car insurance discounts are exclusively available to young drivers under 25 to help them save money. State Farm offers the most savings to students with a 35% discount.

These are the easiest ways to keep your insurance down when teens already have a car they need insurance for. If the teen doesn’t have a vehicle yet, looking at cheap, good cars for teens can also help save you money.

Choosing the Right Vehicle For Cheap Teen Insurance

Most teens will not have brand-new cars. In fact, many experts recommend cars that are between five and seven years old for first-time drivers, as these are often equipped with a number of safety features, like automatic airbags and passenger restraints. They also have updated engine systems that are easier to maintain.

When it’s time to find a teen’s first car, there are several things to look for. Most importantly, it’s a safe vehicle, but you should also look for reliability and affordability. Of course, teens will also appreciate a little bit of style. While there are plenty of choices for cool cars for teens, here are some of the cheapest cars to insure for teenagers:

- Honda Civic: Another popular Honda for teens, the Civic also has stellar safety ratings. As a bonus, the Civic has excellent gas mileage.

- Mazda 3: When it comes to cars for 16-year-olds, the Mazda 3 has solid safety ratings, gas mileage, and affordability. Teens also appreciate Mazda’s sporty drive.

- Subaru Outback: Subaru is well known for its safety and reliability. All of Subaru’s hatchbacks are solid choices, but the Outback is probably the most popular.

- Toyota Camry: When it comes to nice, cheap cars for teens, one of the best choices is the Toyota Camry. The Camry has fantastic safety ratings and a reputation for reliability.

- Ford F-150: If you’re looking for good trucks for 16-year-olds, the Ford F-150 is an excellent option because it has one of the highest safety ratings.

The car insurance industry knows the types of vehicles that have the best safety ratings, like the Honda Civic and the Toyota Camry, and has a good idea of how much these vehicles cost to repair. It is always best to find a durable vehicle with manufacturer’s parts that are easy to locate. Compare auto insurance rates by vehicle make and model to find the cheapest car to insure for teenage drivers.

You must teach your teen to be smart if they ever require maintenance on their vehicles. Replacement parts are part of owning a car, and many auto shops will try to convince you that non-OEM parts are just as safe, but less expensive. The reality is that they may cause more damage. Follow the advice of your car insurance company and only purchase original equipment provided by the manufacturer or OEM parts.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

How to Apply For a Teen Driver’s License

Teens can’t receive a standard driver’s license without completing specific steps, including having an instructional permit and an intermediate driver’s license. Upon completing each step successfully, a teen may apply for a standard driver’s license.

A new driver between 16 and 17 cannot buy auto insurance without a driver's license or learner's permit.Tonya Sisler Insurance Content Team Lead

A graduated driver’s license is a three-part program designed to help teen drivers get their first license, developed by state legislators to help improve driving skills and reduce the risk of motor vehicle accidents.

- Instructional Permit: Known as a learner’s permit, teen drivers must pass vision and written tests and be chaperoned by an adult over 21 with a valid state-approved driver’s license every time they drive.

- Intermediate License: Teens must pass a driver’s education course as established by the Motor Vehicle Commission and the State Board of Education. Most auto insurance companies will require you to provide this information upon requesting a policy.

- Drivers License: Teen drivers must maintain a learner’s and intermediate license for at least 12 months before receiving an official license.

Previously, a teen driver only needed to possess a learner’s permit until they reached the required age. They would then be able to apply for a standard driver’s license. Today, they must complete the intermediate license phase.

The majority of major collisions in the United States occur with drivers between 16 and 20, and graduated license programs help reduce accidents.

Top 10 Companies With The Cheapest Teen Auto Insurance

The only way you’re going to know if you’re getting the cheapest car insurance for a teen driver is to get several quotes from different companies. The companies with the cheapest teen auto insurance on average are USAA, Geico, and State Farm. Compare a variety of insurers, from nationwide corporations to local providers, and see where your best deal is.

Read More: Cheap Auto Insurance For Teens After an Accident

#1 – USAA: Top Pick Overall

Pros

- Cheapest Rates: No matter where you live, USAA likely has the cheapest car insurance for teenagers with military backgrounds.

- Student Discounts: One of the best insurance discounts for teenage drivers to take advantage of is savings for being a good student. You can save up to 10% with USAA by maintaining a good GPA.

- Superb Customer Service: USAA not only offers affordable car insurance for teenage drivers, but it’s also highly rated for its customer service.

Cons

- Eligibility Requirements: Not everyone qualifies for USAA membership — only active or retired military and their families are eligible. Learn how to qualify in our USAA auto insurance review.

- Limited Local Offices: USAA doesn’t have as many local offices as some of its larger competitors, which makes it more difficult to get face-to-face help.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#2 – Geico: Cheapest With Usage-Based Discount

Pros

- DriveEasy Program: Save up to 25% on your policy by enrolling in Geico’s usage-based insurance program, DriveEasy. DriveEasy tracks your driving habits and rewards safe habits with a discount.

- Teen Driver Discounts: Geico offers several ways to get the best car insurance rates for teenage drivers, including excellent discounts. Read our Geico auto insurance review for a list.

- Convenient Digital Tools: Geico makes managing your policy, making payments, and starting claims online easy with its website and mobile app.

Cons

- Claims Satisfaction: Many customers report satisfaction with their Geico policy, but the company does receive a number of complaints about its claims handling.

- Discount Availability Varies: Geico offers a variety of discounts, but availability varies by state.

#3 – State Farm: Cheapest for Safe Drivers

Pros

- Teen Safe Driver Program: Another simple way to find cheap car insurance for 17-year-olds and other teens is to complete the Teen Safe Driver program.

- Drive Safe and Save UBI: You can save up to 30% by enrolling in State Farm’s Drive Safe and Save program and consistently practicing safe habits.

- Student Discounts: State Farm offers a variety of student savings, including the good student, student away at school, defensive driving course, and driver education discounts.

Cons

- Limited Online Tools: State Farm focuses more on providing personalized service, so it lacks some of the online tools you can find with other providers. Learn more in our State Farm auto insurance review.

- Lengthy Claims Process: Despite having fairly solid customer reviews, many complain that the State Farm claims process takes an excessive amount of time to resolve.

#4 – AAA: Cheapest Roadside Assistance Plans

Pros

- Membership Perks: Sign up for AAA to access a variety of member perks, like discounts on shopping and at restaurants. To learn more about membership, visit our AAA auto insurance review.

- Roadside Assistance: If you’re looking for the best car insurance company for teenage drivers with roadside assistance, AAA is famous for having the original roadside assistance plans.

- Solid Customer Service: Not only does AAA offer cheap car insurance for teenage drivers, but it also has excellent customer service ratings.

Cons

- Membership Fees: Drivers need to pay to be an AAA member. While AAA offers cheap car insurance for teens, annual membership fees will increase your costs.

- Coverage Varies by State: AAA insurance is provided by regional clubs, which offer slightly different products and discounts. Make sure to check with a representative to see what’s available in your area.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#5 – Nationwide: Best for Accident Forgiveness

Pros

- Accident Forgiveness: Nationwide offers some of the best car insurance for teenage drivers with accident forgiveness, which won’t raise your rates after the first at-fault claim.

- Diverse Coverage Options: Customize your policy with plenty of add-on options. Check out our Nationwide auto insurance review for all your options.

- SmartRide Program: Nationwide offers a 40% max discount if you sign up for the SmartRide UBI program and regularly practice safe habits.

Cons

- Average Rates: Nationwide doesn’t offer the cheapest insurance for teens, but its rates are also not the highest.

- Limited Availability: You’ll need to check if Nationwide is available in your state, as the company only sells coverage in 47 states.

#6 – American Family: Best for Teen Driving Support

Pros

- Teen Safe Driver program: Completing this program is one of the easiest ways to find the best car insurance for 16-year-olds with exclusive savings.

- Teen Discounts: There are plenty of young driver discounts to take advantage of, including special savings for young volunteers. Explore other discounts in our American Family Insurance review.

- KnowYourDrive program: Save up to 30% on your insurance by signing up for American Family’s UBI program, KnowYourDrive.

Cons

- Not Available Everywhere: American Family is currently available in just 19 states.

- Slow Claims Process: Depending on where you live, American Family may take longer to resolve claims than expected.

#7 – Allstate: Cheapest For Low-Mileage Drivers

Pros

- Milewise and Milewise Unlimited: Allstate offers two pay-per-mile programs to help keep teenage car insurance quotes low. Read our Allstate Milewise review to learn how it works.

- Excellent Coverage Options: Allstate offers some of the best teen car insurance by providing ample coverage options.

- Strong Customer Service Ratings: While it has some complaints, Allstate agents tend to receive excellent customer service reviews for teen car insurance in most states.

Cons

- Higher Rates: Without Milewise discounts, Allstate is usually one of the most expensive teen car insurance companies. See how much you might pay in our Allstate auto insurance review.

- Low Claims Satisfaction: It may have solid customer service reviews, but many policyholders report feeling unsatisfied with Allstate’s online claims resolution.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

#8 – Farmers: Best Discount Selection

Pros

- Long List of Discounts: Farmers offers a whopping 23 discounts to help teen drivers save. To learn more about your discount options, read our Farmers auto insurance review.

- Personalized Service: Farmers focuses more on providing excellent service on teen car insurance through local representatives.

- Solid Add-Ons: There are plenty of options to customize your Farmers policy, including rental car reimbursement and customized equipment coverage for teen auto insurance.

Cons

- Limited Availability: While Farmers used to sell insurance in every state, it no longer offers new policies in Florida. (Read More: Cheapest Teen Driver Auto Insurance in Florida)

- Slow Roadside Assistance: You can add roadside assistance to your Farmers policy, but many customers complain that the service is slow.

#9 – Progressive: Best Online Tools

Pros

- Name Your Price tool: Stay on budget by using the Name Your Price tool. Using this tool generates a list of Progressive coverage options to match your budget.

- Snapshot Program: Drivers who sign up for Progressive’s Snapshot program save an average of $321 per year by practicing safe habits.

- Teen Driver Discounts: Progressive offers several discounts for teens to help keep their rates down. See all of its discounts in our Progressive auto insurance review.

Cons

- Unexpected Rate Increases: Progressive car insurance for teens may start cheap, but many customers complain about inexplicable rate increases.

- Low Customer Loyalty: Despite being one of the largest insurance companies in the country, Progressive struggles with its customer loyalty ratings.

#10 – Travelers: Cheapest for Unique Coverage Options

Pros

- Unique Coverage Options: Travelers offers multiple add-ons you can include in your policy, like rideshare insurance for teen drivers who use their cars for work.

- IntelliDrive UBI Discounts: Safe drivers can save up to 30% on their insurance by enrolling in Travelers’ UBI program, IntelliDrive. Learn more about it in our review of Travelers Insurance.

- Industry Experience: Travelers has reliable teen auto insurance policies backed by over a century of insurance experience and a solid A++ financial rating from A.M. Best.

Cons

- Higher-Than-Average Rates: No matter where you live or what type of driver you are, you’ll likely find lower teen auto insurance rates elsewhere.

- Limited Online Resources: Travelers lacks the online policy management tools that many of its larger competitors offer.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

How to Choose the Cheapest Teen Auto Insurance Company

USAA, Geico, and State Farm are the top three companies with the cheapest teen auto insurance. Teens and young drivers from military families get the best rates with USAA, starting at $146 a month. Learn how auto insurance companies check driving records to lock in the lowest rates for teens.

On the one hand, when your teen 🚗starts driving, you gain freedom. On the other hand, you’ll probably worry😟. https://t.co/27f1xf1ARb can help you find the insurance providers with the best programs for teen drivers. For all the info, check out👉: https://t.co/H1ClPya7QS pic.twitter.com/n5xRX4p3au

— AutoInsurance.org (@AutoInsurance) August 30, 2023

If you need affordable insurance for new drivers, start comparing quotes today by entering your ZIP code into our free online comparison tool to find companies with the cheapest teen auto insurance near you.

Frequently Asked Questions

What are the best auto insurance companies for teens?

USAA, Geico, and State Farm have the best auto insurance rates for teens in most states. Compare State Farm vs. USAA auto insurance for more information and quotes.

What factors should I consider when choosing auto insurance for my teen?

When selecting auto insurance for your teen, it’s essential to consider the cost, deductible options, customer service, and any teen-specific programs or incentives a company offers for young drivers, such as student discounts, UBI, or defensive driving courses.

Do auto insurance rates for teens tend to be higher than rates for other age groups?

Generally, auto insurance rates for teen drivers are higher than those for other age groups. Teenagers are statistically more likely to be involved in accidents due to their limited driving experience. However, many insurance companies offer discounts and programs specifically designed to help lower rates for teen drivers. Enter your ZIP code to find cheap teen auto insurance near you.

Are there any discounts available for teen drivers?

Yes, several insurance companies provide discounts to help reduce insurance costs for teen drivers. Some common discounts include good student discounts, driver training discounts, safe driving rewards, and multi-vehicle discounts for families who insure more than one car with a single policy.

Can I add my teen driver to my existing auto insurance policy, or do they need their own policy?

In most cases, you have the option to add your teen driver to your existing auto insurance policy. This is often the most convenient and cost-effective choice. However, depending on your insurance company and policy terms, there may be situations where it’s more beneficial or required to have a separate policy for your teen driver.

What car has the cheapest insurance for teenagers

Does the car a teen drives affect auto insurance? Yes, and the cheapest car for a teen to insure depends on several factors, but insurance companies give the best rates to vehicles with solid safety and reliability ratings. That means brands like Toyota, Honda, and Subaru tend to have low rates.

What are the companies with the cheapest teen auto insurance?

USAA, Geico, and State Farm have the lowest average rates for teen drivers.

Why do teen drivers pay more for auto insurance?

Teens see some of the highest average rates for a few reasons. Generally, teens are more likely to cause accidents, engage in reckless behaviors, and drive distracted. They’re also less equipped to deal with the dangers of the road, such as black ice and inclement weather.

How can teens save on their insurance?

If you’re looking for the lowest possible teen car insurance rates, ask about discounts, enroll in a UBI program, choose minimum coverage, maintain a clean driving record, and complete a driver’s education course. Learn how to get a defensive driver auto insurance discount.

When do teen auto insurance rates go down?

As long as you keep your driving record clean of at-fault accidents, speeding tickets, and other traffic violations, your insurance rates should decrease by the time you’re 25.

Related Articles

-

Jul 2025

Best Auto Insurance for Hybrid Vehicles in 2026 (Your Guide to the Top 10 Companies)

-

Feb 2025

Does owning a home affect auto insurance rates? (2026)

-

Aug 2025

Best Driver’s Ed Auto Insurance Discounts in 2026 (Save up to 20% With These 10 Companies)

-

Dec 2024

How to Research Auto Insurance Companies in 2026 (Follow These 5 Steps)

-

Aug 2025

8 Best Auto Insurance Companies for Drivers With Speeding Tickets (Top Providers Ranked in 2026)

-

Dec 2024

What is a good deductible for auto insurance?

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.