Do you need insurance on a car that doesn’t run?

Are you wondering: "Do you need insurance on a car that doesn't run?" Most states will require you to have insurance if you want to drive and insure it in the future. You can save money by reducing coverage to the state minimum or switching to a usage-based policy.

Read more

Table of Contents

Table of Contents

Insurance and Finance Writer

Laura Gunn is a former teacher who uses her passion for writing and learning to help others make the best decisions regarding finance and insurance. After stepping away from the classroom, Laura used her skills to write across many different industries including insurance, finance, real estate, home improvement, and healthcare. Her experience in various industries has helped develop both her ...

Laura Gunn

Licensed Insurance Agent

Tim Bain is a licensed insurance agent with 23 years of experience helping people protect their families and businesses with the best insurance coverage to meet their needs. His insurance expertise has been featured in several publications, including Investopedia and eFinancial. He also does digital marking and analysis for KPS/3, a communications and marking firm located in Nevada.

Tim Bain

Updated October 2024

If you have a vehicle that doesn’t run and you have full coverage auto insurance, you might wonder whether you have to keep insurance on a car you don’t drive. It’s important to know whether or not you need insurance on a car that doesn’t run.

Nobody wants to overpay for auto insurance. This article will cover whether or not you should have car insurance for a car that doesn’t run, how to get auto insurance without a car, and more.

Continue scrolling to find out if you you have to have insurance on a car that doesn’t run or enter your ZIP code above to get free quotes from the top auto insurance companies in your area.

- Most states require vehicles to remain insured whether they run or not

- It might be a good idea to get usage-based auto insurance if you need to continue insuring a car that doesn’t run

- For those without a car, non-owner auto insurance is a good option to keep you covered while driving other cars or shopping for a new car

Insurance for Cars That Aren’t Driven

The short answer is yes, you most likely do need insurance for a non operational vehicle. That said, there are some shades of grey. In short, you will need auto insurance on any vehicle that you intend on driving and insuring in the future, even if it doesn’t run now.

This can be frustrating if you have an inoperable vehicle and have since bought another car to drive indefinitely. In many cases, you will be required to maintain an auto insurance policy on a car even if it is in storage.

If you have a car that doesn’t run and you’re considering your options for insurance on non operational vehicles, you will have a few things to consider. Some of these factors include your desire to drive the vehicle in the future, the reason it’s inoperable, the state you live in, and whether or not you are driving another vehicle in the meantime.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

If I Don’t Drive my Car Do I Need Insurance

As mentioned previously, your car will need insurance if not being used. This also means that you, as a potential driver, will need to maintain your auto insurance.

Realistically, it’s easier to just maintain your auto insurance policy considering the inconveniences of needing to reinstate an auto insurance policy last minute if something were to come up.

We get it, many people live in a city where driving is a bigger hassle than it’s worth. Even so, you would want to keep your insurance for yourself and to protect your vehicle. If you live in the city, it could be increasingly important to have comprehensive insurance on a car, even if it doesn’t run.

Between the narrow roads and excessive traffic, your car is likely exposed to many risks and could be damaged in the city streets. If your car doesn’t run but is still cosmetically appealing, you would want to keep it protected.

Registering a Car That Doesn’t Run

So, do you have to register a non-running car? You will be required to register a non-operable vehicle in most states. For example, according to the Florida Department of Highway Safety and Motor Vehicles, despite registration, a non-running vehicle need to be insured in Florida. Unfortunately, this would also include vehicles that don’t run.

Can I drive a non op car in California? Some states, such as California, have specific forms you can complete to acknowledge that the vehicle is inoperable. This Certified of Non-operation can be found on the Department of Motor Vehicles website and may offer some financial benefits with your insurer.

Otherwise, it’s probably best to keep your vehicle registered regardless of its ability to drive, assuming you want to drive it again in the future.

Car Insurance for Non-Operating Vehicles

While you should most likely keep your car insured, that doesn’t mean that you need the same exact insurance on the car. In fact, non op cars do need insurance that meets your state’s minimum auto insurance requirements.

Auto Insurance Minimum Requirements by State

| State | Liability Limits | Required Coverages |

|---|---|---|

| Alabama | 25/50/25 | Bodily Injury Liability, Property Damage Liability |

| Alaska | 50/100/25 | Bodily Injury Liability, Property Damage Liability |

| Arizona | 15/30/10 | Bodily Injury Liability, Property Damage Liability |

| Arkansas | 25/50/25 | Bodily Injury Liability, Property Damage Liability, Personal Injury Protection |

| California | 15/30/5 | Bodily Injury Liability, Property Damage Liability |

| Colorado | 25/50/15 | Bodily Injury Liability, Property Damage Liability |

| Connecticut | 25/50/20 | Bodily Injury Liability, Property Damage Liability, Uninsured Motorist Coverage, Underinsured Motorist Coverage |

| Delaware | 25/50/10 | Bodily Injury Liability, Property Damage Liability, Personal Injury Protection |

| Florida | 25/50/10 | Bodily Injury Liability, Property Damage Liability, Personal Injury Protection |

| Georgia | 10/20/10 | Bodily Injury Liability, Property Damage Liability |

| Hawaii | 25/50/25 | Bodily Injury Liability, Property Damage Liability, Personal Injury Protection |

| Idaho | 20/40/10 | Bodily Injury Liability, Property Damage Liability |

| Illinois | 25/50/15 | Bodily Injury Liability, Property Damage Liability, Uninsured Motorist Coverage, Underinsured Motorist Coverage |

| Indiana | 25/50/20 | Bodily Injury Liability, Property Damage Liability |

| Iowa | 25/50/25 | Bodily Injury Liability, Property Damage Liability |

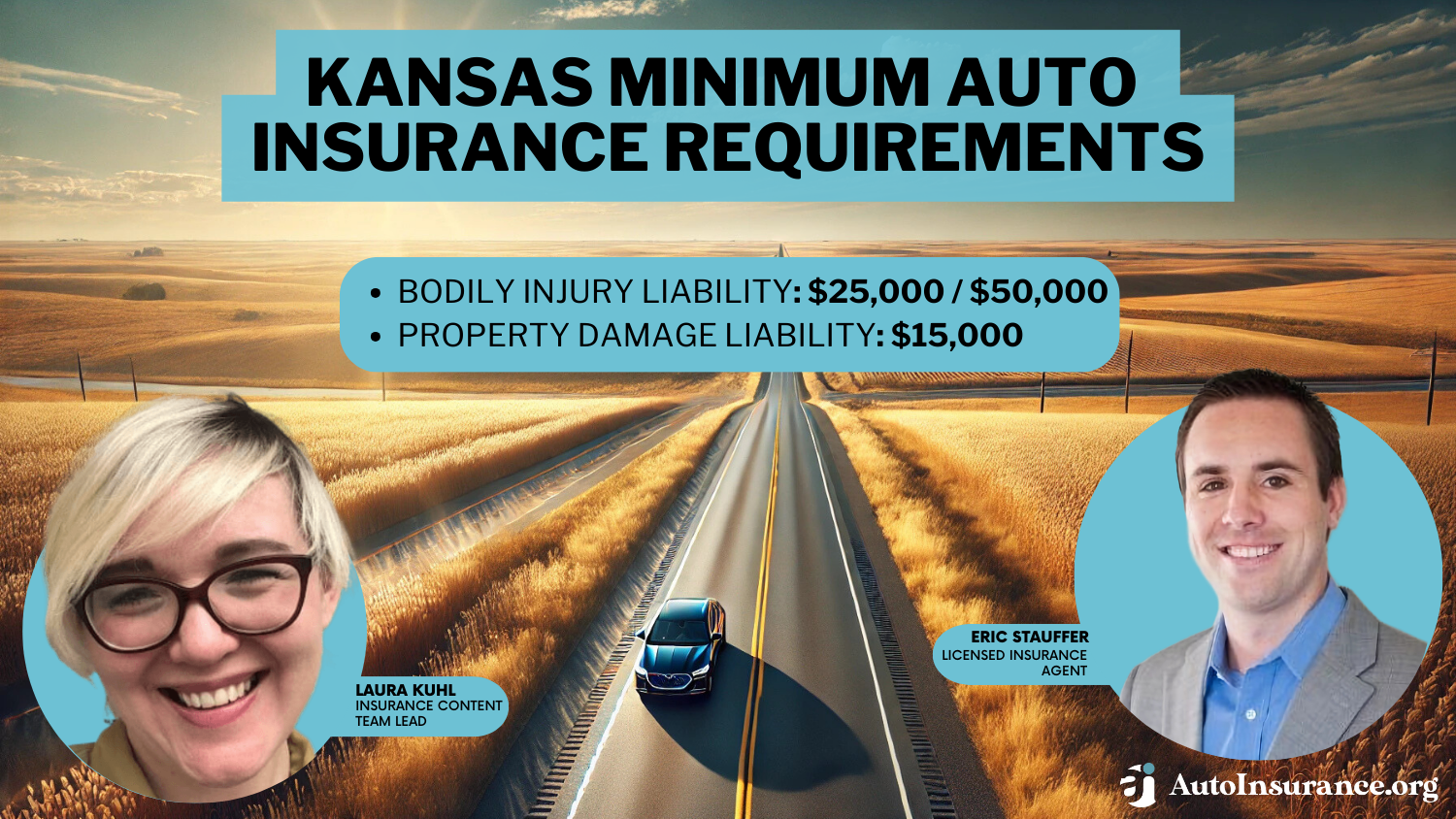

| Kansas | 20/40/15 | Bodily Injury Liability, Property Damage Liability, Personal Injury Protection |

| Kentucky | 25/50/25 | Bodily Injury Liability, Property Damage Liability, Personal Injury Protection, Uninsured Motorist Coverage, Underinsured Motorist Coverage |

| Louisiana | 25/50/25 | Bodily Injury Liability, Property Damage Liability |

| Maine | 15/30/25 | Bodily Injury Liability, Property Damage Liability, Uninsured Motorist Coverage, Underinsured Motorist Coverage, Medical Payments Coverage |

| Maryland | 50/100/25 | Bodily Injury Liability, Property Damage Liability, Personal Injury Protection, Uninsured Motorist Coverage, Underinsured Motorist Coverage |

| Massachusetts | 30/60/15 | Bodily Injury Liability, Property Damage Liability, Personal Injury Protection |

| Michigan | 20/40/5 | Bodily Injury Liability, Property Damage Liability, Personal Injury Protection |

| Minnesota | 20/40/10 | Bodily Injury Liability, Property Damage Liability, Personal Injury Protection, Uninsured Motorist Coverage, Underinsured Motorist Coverage |

| Mississippi | 30/60/10 | Bodily Injury Liability, Property Damage Liability |

| Missouri | 25/50/25 | Bodily Injury Liability, Property Damage Liability, Uninsured Motorist Coverage |

| Montana | 25/50/25 | Bodily Injury Liability, Property Damage Liability |

| Nebraska | 25/50/20 | Bodily Injury Liability, Property Damage Liability, Uninsured Motorist Coverage, Underinsured Motorist Coverage |

| Nevada | 25/50/25 | Bodily Injury Liability, Property Damage Liability |

| New Hampshire | 25/50/20 | Financial Responsibility only |

| New Jersey | 25/50/25 | Bodily Injury Liability, Property Damage Liability, Personal Injury Protection, Uninsured Motorist Coverage, Underinsured Motorist Coverage |

| New Mexico | 15/30/5 | Bodily Injury Liability, Property Damage Liability |

| New York | 25/50/10 | Bodily Injury Liability, Property Damage Liability, Personal Injury Protection, Uninsured Motorist Coverage, Underinsured Motorist Coverage |

| North Carolina | 25/50/10 | Bodily Injury Liability, Property Damage Liability, Uninsured Motorist Coverage, Underinsured Motorist Coverage |

| North Dakota | 30/60/25 | Bodily Injury Liability, Property Damage Liability, Personal Injury Protection, Uninsured Motorist Coverage, Underinsured Motorist Coverage |

| Ohio | 25/50/25 | Bodily Injury Liability, Property Damage Liability |

| Oklahoma | 25/50/25 | Bodily Injury Liability, Property Damage Liability |

| Oregon | 25/50/25 | Bodily Injury Liability, Property Damage Liability, Personal Injury Protection, Uninsured Motorist Coverage, Underinsured Motorist Coverage |

| Pennsylvania | 25/50/20 | Bodily Injury Liability, Property Damage Liability, Personal Injury Protection |

| Rhode Island | 15/30/5 | Bodily Injury Liability, Property Damage Liability |

| South Carolina | 25/50/25 | Bodily Injury Liability, Property Damage Liability, Uninsured Motorist Coverage, Underinsured Motorist Coverage |

| South Dakota | 25/50/25 | Bodily Injury Liability, Property Damage Liability, Uninsured Motorist Coverage, Underinsured Motorist Coverage |

| Tennessee | 25/50/25 | Bodily Injury Liability, Property Damage Liability |

| Texas | 25/50/15 | Bodily Injury Liability, Property Damage Liability, Personal Injury Protection |

| Utah | 30/60/25 | Bodily Injury Liability, Property Damage Liability, Personal Injury Protection |

| Vermont | 25/65/15 | Bodily Injury Liability, Property Damage Liability, Uninsured Motorist Coverage, Underinsured Motorist Coverage |

| Virginia | 25/50/10 | Bodily Injury Liability, Property Damage Liability, Uninsured Motorist Coverage, Underinsured Motorist Coverage |

| Washington | 25/50/20 | Bodily Injury Liability, Property Damage Liability |

| Washington, D.C. | 25/50/10 | Bodily Injury Liability, Property Damage Liability, Uninsured Motorist Coverage |

| West Virginia | 25/50/25 | Bodily Injury Liability, Property Damage Liability, Uninsured Motorist Coverage, Underinsured Motorist Coverage |

| Wisconsin | 25/50/10 | Bodily Injury Liability, Property Damage Liability, Uninsured Motorist Coverage, Medical Payments Coverage |

| Wyoming | 25/50/20 | Bodily Injury Liability, Property Damage Liability |

If your car doesn’t run, there’s a good chance that it isn’t worth very much in most cases. Assuming that’s the case, you can probably settle for a low-cost auto insurance policy with your state’s minimum coverage. As you can see above, these values vary drastically from state to state.

Otherwise, you could also consider a usage-based auto insurance policy. These policies aren’t always recommended, but if you have a car that can’t be driven, you’ll clearly have very low usage on that vehicle.

Some auto insurance companies will allow policyholders to purchase usage-based insurance on only one car whereas others may require policyholders to enroll all vehicles, so this is another factor to consider. Pay-per-mile auto insurance would likely be one of the most affordable options if you have a car that doesn’t run that you need to insure.

Can I get auto insurance without a car?

If your car is no longer running and you don’t care if it ever drives on the road again, you won’t need to keep it insured. You will need to find a way to get rid of the vehicle so that it doesn’t rot in your driveway, but it’s up to you how you’ll dispose of it.

Enter your ZIP code below to view companies that have cheap auto insurance rates.Free Auto Insurance Comparison

If you no longer have a car but you’re in the shopping process or you’re looking to get your first car, you might need to know how to get auto insurance without a car. Thankfully, this is a straightforward process.

To get auto insurance without a car, you’ll need to ask your insurance company about non-owner auto insurance. These insurance policies also tend to use the state minimums for coverage, unless otherwise requested. This will allow you to stay covered if you drive vehicles owned by friends or at work.

If you’re considering this type of insurance, you’ll want to be sure to get quotes from multiple insurers to see which company offers the best rates.

Buying Insurance for a Car That Doesn’t Run: The Bottom Line

Do I need insurance if i don’t drive my car? In most cases, a non op car will need insurance. It’s required to keep all vehicles registered and insured if you intend on ever driving the vehicle again. There are some auto insurance options to help save in the meantime.

By now, you should have a better understanding of how to get insurance for a car that doesn’t run. Before you go, enter your ZIP code below to get free quotes from the cheapest auto insurance companies in your area.

Frequently Asked Questions

Does my car need insurance if i’m not driving it?

So, do you still have to have insurance on a non-operational vehicle? You generally need insurance on a car that doesn’t run, although the specific requirements may vary depending on your location and local regulations. Even if the car is inoperable and not being driven, it could still be exposed to certain risks or liabilities.

Why do I need inoperable vehicle insurance?

There are several reasons why you might be required to have non op car insurance:

- Protection against theft or vandalism: Insurance can help cover the cost of repairs or replacement if your non-running car is stolen or vandalized.

- Liability coverage: If your non-running car causes damage to another person’s property or injures someone while parked, you could be held financially responsible. Insurance can provide liability coverage to protect you in such situations.

- Storage-related risks: Non-running cars can be susceptible to risks such as fire, flooding, or damage from falling objects. Insurance can help cover the costs of these damages.

What type of insurance coverage do I need for a non-running car?

The type of insurance coverage you need for a non-running car may depend on your specific situation and local regulations. Here are some common coverage options:

- Comprehensive coverage: This coverage protects against theft, vandalism, and damage caused by events other than accidents, such as fire, flood, or falling objects.

- Storage coverage: Some insurers offer specialized storage or “inoperable vehicle” coverage designed for non-running cars. This coverage may be more affordable since the car is not being driven.

- Liability coverage: Liability coverage is essential if your non-running car poses a risk of causing property damage or bodily injury to others while parked.

Do you have to pay insurance on a non op car or can you suspend your coverage?

It depends on the insurance company and your policy terms. Some insurers may allow you to suspend coverage temporarily if you can provide proof that the car is inoperable and won’t be driven. However, it’s important to check with your insurance provider to understand their specific guidelines and any potential consequences of suspending coverage.

Are there any consequences for not insuring a non-running car?

Yes, there can be consequences for not insuring a non-running car, especially if it’s required by law or if you want to protect yourself from potential liabilities. Operating an uninsured vehicle, even if it doesn’t run, could result in fines, penalties, or legal issues depending on your jurisdiction.

Can I remove my non-running car from my existing auto insurance policy?

In many cases, you can remove a non-running car from your existing auto insurance policy. Contact your insurance provider to inform them about the situation and discuss your options. They may be able to adjust your policy accordingly, either by removing the car entirely or switching it to a different type of coverage that suits its non-operational status.

Will non-operable car insurance costs be lower than the costs of insuring a functioning vehicle?

Generally, insuring a non-running car can be more affordable than insuring a functioning vehicle. Since the car is not being driven, the risk of accidents or collisions is significantly reduced. Insurance providers may offer specialized coverage options or reduced rates for non-running cars. However, the actual cost will depend on various factors, including your location, the car’s value, and the specific coverage you choose.

Can I transfer my existing insurance coverage from a running car to a non-running car?

In most cases, you cannot transfer the insurance coverage from a running car directly to a non-running car. Insurance policies are typically vehicle-specific, and coverage needs to be adjusted accordingly. You will likely need to inform your insurance provider about the change in vehicles and request appropriate coverage for the non-running car.

What documentation might be required to insure a non-running car?

While the documentation requirements can vary depending on the insurance provider and your location, some common documents you may need to provide include:

- Vehicle identification number (VIN)

- Proof of ownership, such as the car’s title or registration documents

- Information about the car’s condition and reasons for it being non-running

- Any relevant storage or parking details

Can I cancel insurance on a non-running car if I plan to sell or dispose of it soon?

If you plan to sell or dispose of the non-running car in the near future, you may be able to cancel the insurance coverage once you no longer own it. However, it’s essential to check with your insurance provider regarding their cancellation policies and any potential fees or requirements associated with terminating the coverage.

What to do with a car that doesn’t run?

How do you know if your car is broken down?

My car broke down on the highway, what should I do?

Does a non op car need insurance in California?

How do I register a non-operational vehicle in California?

What does PNO mean?

How much does insurance cost for a car that doesn’t run?

Does my car need insurance if I’m not driving it in Ohio?

Do you need insurance for non-operational vehicles in Nevada?

Can I take insurance off my car if I’m not driving it in Arizona?

Can you pause your car insurance with Geico if you’re not driving the vehicle?

Do I need car insurance if I don’t drive my car in Illinois?

What does it mean when a car is not operable?

What is the difference between operable and inoperable?

My car broke down who do I call?

What is the cost of car storage insurance?

How long can car insurance lapse in Florida?

Do I need insurance on a car that is broken down?

Can I take insurance off my car if i’m not driving it in Florida?

Related Articles

-

Apr 2026

Do I need to know auto insurance company codes?

-

Jan 2025

Best Business Auto Insurance in 2026 (Check Out the Top 10 Providers)

-

Mar 2025

Washington Minimum Auto Insurance Requirements for 2026 (Coverage WA Drivers Need)

-

Mar 2025

Kansas Minimum Auto Insurance Requirements in 2026 (KS Coverage Details)

-

Dec 2024

Do you need proof of insurance to rent a car?

-

Dec 2024

Who governs Florida auto insurance companies?

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.